Are Student Loans Tax Deductible? A Guide to the 1098-E and Beyond

Key Terms in This Article

- Above-the-Line Deduction

- A tax deduction that is subtracted from your total gross income to determine your Adjusted Gross Income (AGI). You can claim these even if you do not itemize your deductions.

- Adjusted Gross Income (AGI)

- Your total income minus specific 'above-the-line' adjustments. This figure is used to determine your eligibility for various tax credits and benefits, including Trump Accounts.

- Form 1098-E

- The official 'Student Loan Interest Statement' provided by your loan servicer if you paid $600 or more in student loan interest during the year.

- Modified Adjusted Gross Income (MAGI)

- A calculation used by the IRS to determine if you qualify for certain tax benefits, such as the student loan interest deduction phase-out.

- Qualified Education Loan

- Any debt incurred solely to pay for higher education expenses for yourself, your spouse, or your dependent. This includes most federal and private student loans, but excludes loans from relatives or retirement plans.

- Trump Account

- A new tax-advantaged savings tool for children established by the One Big Beautiful Bill Act. For eligible children born between 2025 and 2028, the government provides a $1,000 treasury contribution to kick-start the account.

Table of Contents

Key Takeaways

I. Introduction

II. Maximizing Your Student Loan Interest Deduction

- Which Student Loans Are Tax Deductible? Federal vs. Private Rules

- Can I Claim Student Loans On My Taxes Without the 1098-E Form?

- Step-by-Step: Finding Your 1098-E on Nelnet and Aidvantage

III. Do Student Loans Count as Income? Your 2026 Refund Guide

- How Student Loans Affect Your Tax Refund and How to Protect It

- 2026 Alert: The 2026 Refund Shield

IV. Advanced Tax Planning: Student Loans and FAFSA

- Will Student Loans Affect FAFSA Eligibility Next Year?

- Reporting Forgiven Student Loans As Income: The “Tax Bomb” Guide

- The 1040 Advantage: Lowering AGI to Qualify for Trump Accounts

V. Frequently Asked Questions

VI. Conclusion

Key Takeaways

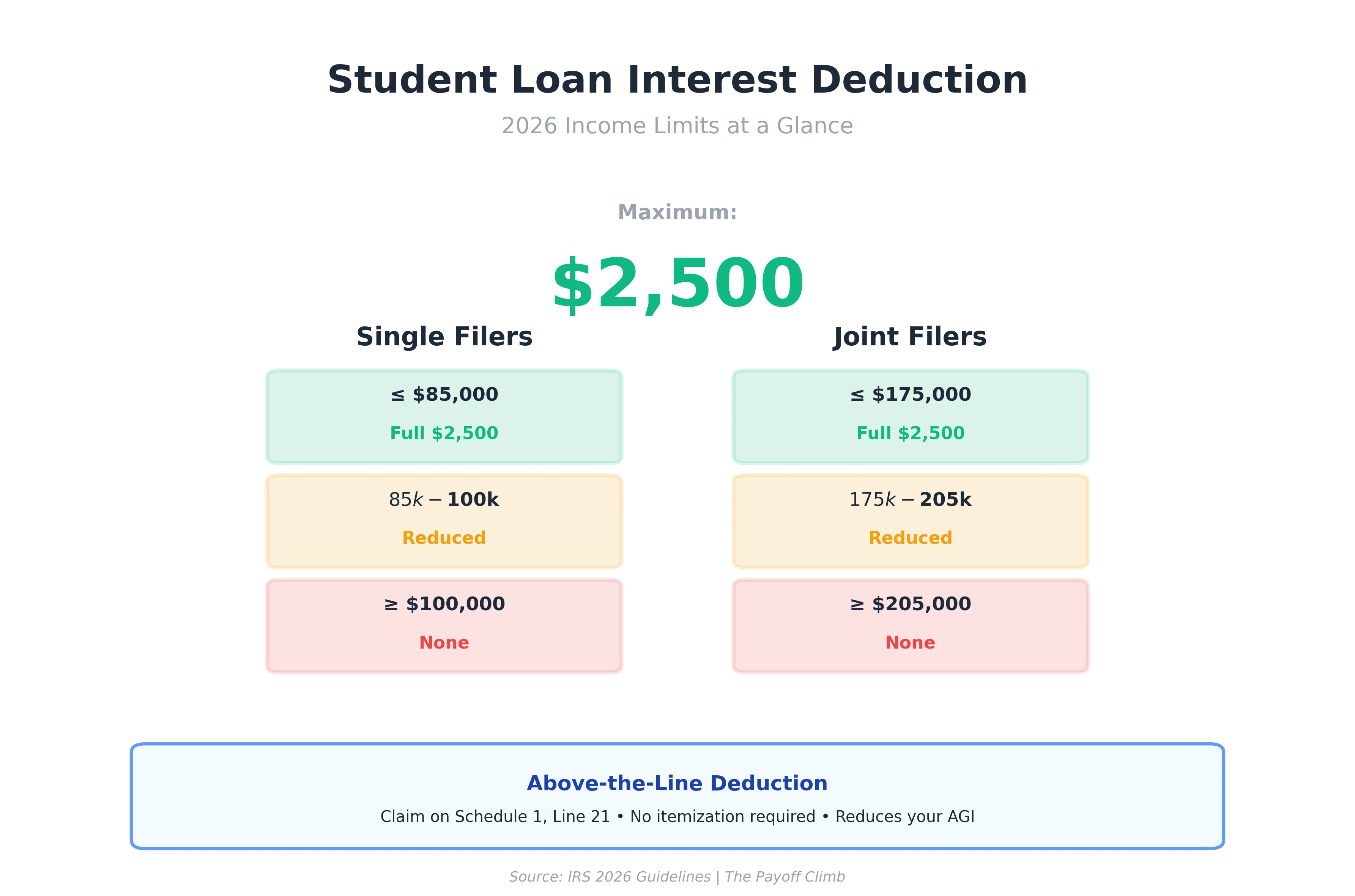

- Maximum Deduction: You can deduct up to $2,500 of the student loan interest paid for the year on your 2026 tax return.

- Liability Status: Student loans are considered a liability because they must be repaid; therefore, the loan proceeds themselves are not considered income for tax purposes.

- 2026 Income Phase-Outs: The deduction begins to disappear at a MAGI of $85,000 for single filers and $175,000 for joint filers. It is completely unavailable once income hits $100,000 (single) or $205,000 (joint).

- Interest Structure: While student loans typically accrue interest, the IRS allows for the deduction of both required and voluntarily prepaid interest payments.

- The 2026 “Tax Bomb”: Federal tax exemptions for forgiven student loans expire at the end of 2025. Starting in 2026, debt discharged under certain repayment plans may be treated as taxable income.

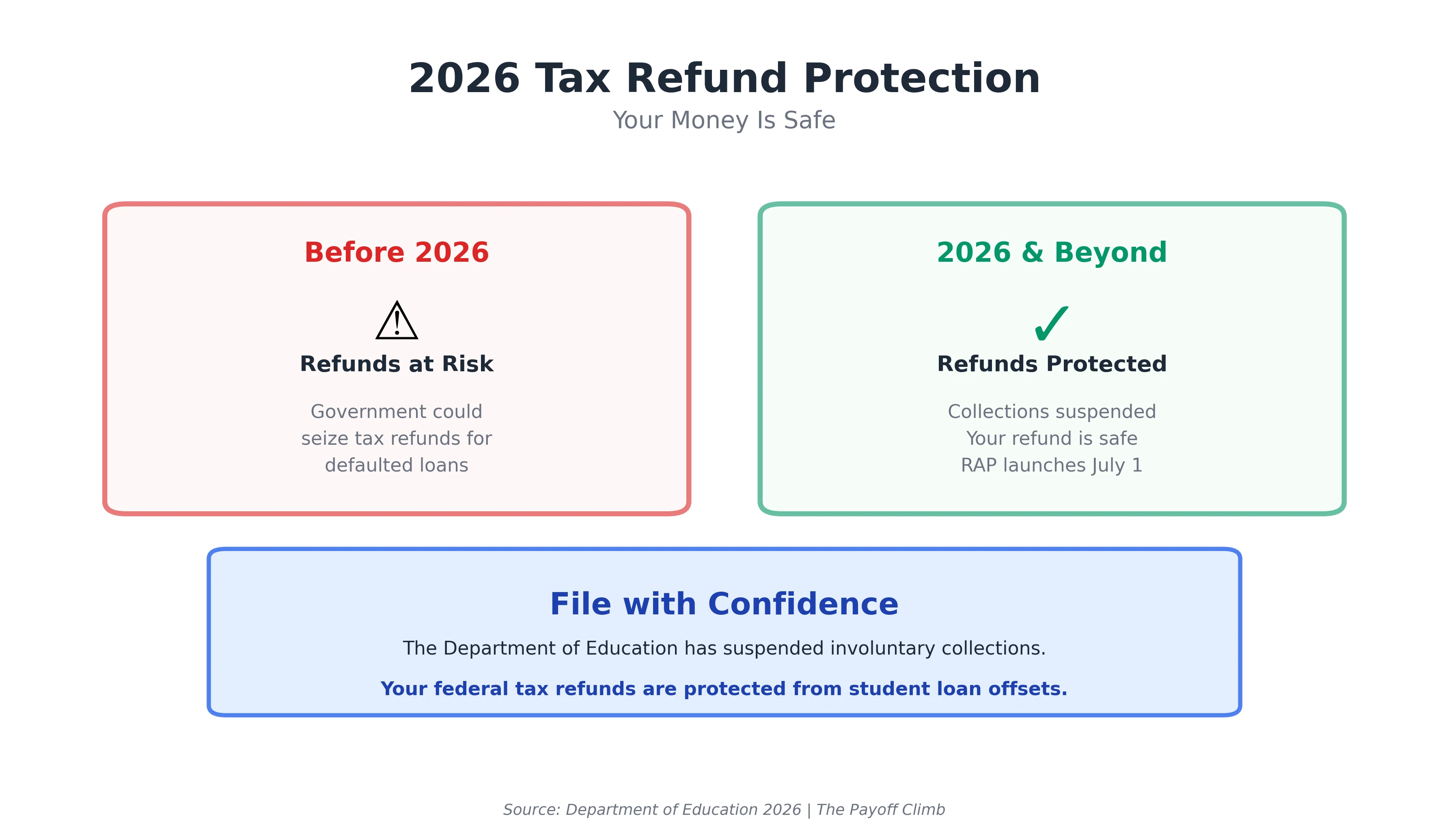

- Refund Protection: Federal tax refunds are currently shielded from seizure (offsets) for defaulted student loans through 2026 as part of the transition to the new Repayment Assistance Program (RAP).

I. Introduction

For millions of Americans, the arrival of January brings a familiar scavenger hunt for tax forms, with the 1098-E Student Loan Interest Statement often sitting at the top of the pile. As we navigate the 2026 tax season, understanding how student loans affect taxes is a critical part of year-end planning that can directly lower your tax bill.

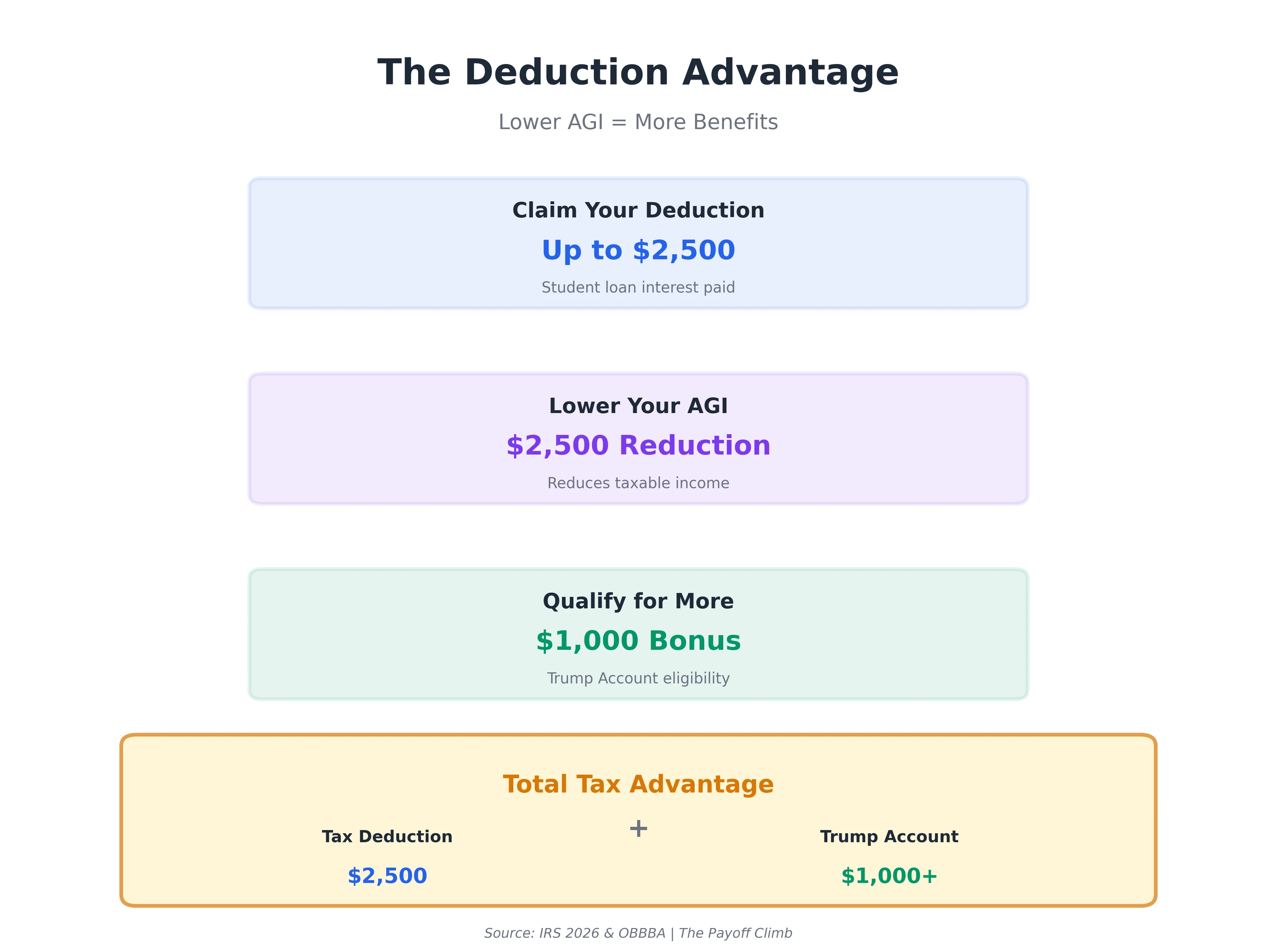

For the 2026 tax year, the IRS continues to allow eligible borrowers to deduct the lesser of $2,500** or the actual student loan interest paid for the year. This is an “above-the-line” deduction, meaning you don’t need to itemize your taxes to claim it. It directly reduces your Adjusted Gross Income (AGI), which can potentially qualify you for other federal benefits like the newly launched Official Trump Account Guidance for children.

Whether you are paying off federal or private student loans, this guide will walk you through the line-by-line 1040 requirements and the specific 2026 regulatory changes you need to know to maximize your return.

II. Maximizing Your Student Loan Interest Deduction

Effective student loan year-end tax planning requires understanding the strict mechanics of the deduction. To claim this benefit, you must enter your total eligible interest on line 21 of Schedule 1 on Form 1040. This amount is then carried over to reduce your total income before you reach your AGI.

Qualifying for the full student loan interest deduction limit 2026 depends on your Modified Adjusted Gross Income (MAGI). For 2026, the student loan interest deduction phase out begins at $85,000 for single filers and $175,000 for those married filing jointly.

| 2026 Filing Status | Full $2,500 Deduction | Partial Deduction Phase-Out | No Deduction Allowed |

|---|---|---|---|

| Single / Head of House | MAGI ≤ $85,000 | $85,001 – $99,999 | MAGI ≥ $100,000 |

| Married Filing Jointly | MAGI ≤ $175,000 | $175,001 – $204,999 | MAGI ≥ $205,000 |

Table 1: 2026 Student Loan Interest Phase-Out Limit.

Which Student Loans Are Tax Deductible? Federal vs. Private Rules

When determining which student loans are tax deductible, the IRS broadly includes any “qualified education loan” used solely for higher education expenses.

- Federal vs. Private: You can generally claim interest on private loans just as you would for federal ones, provided the lender is not a relative or a tax-advantaged retirement plan.

- Consolidation and Refinancing: Deductions are maintained for both consolidated loans and refinanced loans, as long as the original debt was for qualified education.

- Parent PLUS and Advanced Degrees: Parents can claim the deduction for Parent PLUS loans if the loan is in their name and they paid the interest. Interest paid for graduate school or study abroad is also eligible if the student was at an eligible institution.

Can I Claim Student Loans On My Taxes Without the 1098-E Form?

If you paid at least $600 in interest during the year, your student loan service providers are federally required to send you a copy of Form 1098-E. If you paid less than $600, you can still report student loans on taxes, but you will need to manually calculate the interest from your monthly statements.

Step-by-Step: Finding Your 1098-E on Nelnet and Aidvantage

To find your loan servicer, you can check your StudentAid.gov dashboard. You can also consult the StudentAid.gov 1098-E Guide for direct assistance.

- Nelnet: Nelnet tax forms 2026 are typically available in the “Tax Information” section of your online account by January 31.

- Aidvantage: Retrieve your 1098-E electronic copy via the “Interest and Taxes” portal.

III. Do Student Loans Count as Income? Your 2026 Refund Guide

Are student loans considered income? Generally, no, because the money must be repaid. However, 2026 introduces a significant shift for those receiving loan forgiveness, as temporary exemptions are ending.

How Student Loans Affect Your Tax Refund and How to Protect It

Your student loans primarily affect your refund by providing the student loan interest deduction, which lowers your taxable income. By claiming up to $2,500 on line 21 of Schedule 1, you lower your AGI, which can lead to a larger refund.

2026 Alert: The 2026 Refund Shield

Why Your Taxes are Safe from Seizure

-

For 2026, the Department of Education has maintained an indefinite suspension of involuntary collections, including tax refund offsets, for federal student loans in default. As the government transitions to the new Repayment Assistance Program (RAP) launching July 1, 2026, borrowers are currently protected from student loan-related seizures.

IV. Advanced Tax Planning: Student Loans and FAFSA

For families and high earners, student loan year-end tax planning requires a look at broader eligibility. Parents can deduct interest for a child’s loan only if the loan is in the parent’s name. You cannot claim the deduction if you are claimed as a dependent on someone else’s return. Additionally, the deduction is prohibited for those using the married filing separately status.

Will Student Loans Affect FAFSA Eligibility Next Year?

- Because the student loan interest deduction is an “above-the-line” adjustment, it reduces your AGI. Since federal financial aid through FAFSA is based on AGI, lowering this figure today can potentially increase your eligibility for need-based aid in future academic years.

Reporting Forgiven Student Loans As Income: The “Tax Bomb” Guide

- The temporary federal tax exemption for forgiven student debt expires at the end of 2025. For the 2026 tax year, debt discharged under Income-Driven Repayment (IDR) plans may once again be treated as taxable income, unless the borrower qualifies for permanent exceptions such as Public Service Loan Forgiveness (PSLF).

The 1040 Advantage: Lowering AGI to Qualify for Trump Accounts

- The 2026 tax year introduces Trump Accounts, a savings tool established by the One Big Beautiful Bill Act. The government provides a one-time $1,000 contribution for eligible children born between 2025 and 2028.

- By claiming the student loan interest deduction, you lower your AGI, which can help you stay under income thresholds required to qualify your child for this $1,000 federal deposit.

| Savings Feature | Trump Account (2026 Pilot) | Traditional 529 Plan |

|---|---|---|

| Initial Federal Seed | $1,000 (for kids born 2025-28) | $0 |

| Annual Private Limit | $5,000 total per child | Varies by State |

| Launch Date | July 4, 2026 | Currently Available |

| K-12 Distributions | Not Applicable | Up to **$20,000/year** |

Table 2: Savings Comparison: Trump Account vs. 529 Plan (2026)

V. Frequently Asked Questions

Q: Are student loans tax deductible in 2026?

A: Yes, for the 2026 tax year, you can deduct the lesser of $2,500 or the actual student loan interest paid for the year. This is an “above-the-line” deduction that reduces your AGI. It phases out entirely for single filers once MAGI reaches $100,000.

Q: Can I claim student loan interest on my taxes without a 1098-E form?

A: Yes. While lenders only send Form 1098-E if you paid $600 or more in interest, you are still eligible to deduct interest below that amount. You must manually calculate the total interest from your monthly statements to report it accurately.

Q: Are student loans considered taxable income?

A: No, loan proceeds are not considered income because they must be repaid. However, starting in 2026, forgiven student debt may be treated as taxable income due to the expiration of temporary federal exemptions.

Q: How do student loans affect my tax refund?

A: Student loans generally increase your tax refund by lowering your taxable income through the interest deduction. Reducing your AGI may also help you qualify for credits or the new Trump Accounts treasury contribution.

Q: Where is the student loan interest deduction on the 1040?

A: For the 2026 filing season, claim this deduction on line 21 of Schedule 1 on Form 1040. Because it is an adjustment to income, you do not need to itemize your deductions to receive this benefit.

VI. Conclusion

Navigating student loans during the 2026 tax season requires balancing traditional deductions with historic new opportunities. By maximizing the $2,500 student loan interest deduction on your 1040, you don’t just lower your immediate tax bill, you strategically reduce your AGI. This reduction acts as a gateway to qualify for the $1,000 government contribution into the newly launched Trump Accounts for your children.

As the “Tax Bomb” for forgiven loans returns and programs like the Repayment Assistance Program (RAP) begin their rollout on July 1, 2026, staying informed is your best defense against unexpected costs. Use this year’s filing as a foundation for long-term wealth building, ensuring every dollar of interest paid works toward a more secure financial future.

Your debt may be a hurdle, but with the right tax strategy, it can also be the key that unlocks a new generation of savings.