Can Student Loans Be Discharged in Bankruptcy? The 2026 Reality

Key Terms in This Article

- Adversary Proceeding

- A formal 'lawsuit within a bankruptcy' required to prove that your student loans meet the undue hardship standard for discharge.

- Attestation Form

- A standardized affidavit used by the DOJ in 2026 to evaluate a borrower's financial hardship based on objective IRS standards.

- Brunner Test

- The traditional three-part legal test (Ability to Pay, Persistence, and Good Faith) used by most courts to decide if a student loan should be discharged.

- Co-debtor Stay

- A legal protection in Chapter 13 bankruptcy that prevents creditors from collecting from your cosigner while your repayment plan is active.

- TPD Discharge

- A 'Total and Permanent Disability' discharge that cancels federal student loans for borrowers with medically verified impairments lasting at least 5 years.

- Undue Hardship

- The legal standard a borrower must meet to show that repaying student loans would prevent them from maintaining a minimal standard of living.

Table of Contents

Key Takeaways: What You Need to Know in 2026

I. Introduction

- Understanding the Success Rates: The Shift Since 2022

II. The Brunner Test and the New “Undue Hardship” Standards

- Why student loans are not traditionally discharged and how it is changing

- Proving undue hardship in court: Step-by-step

III. The Legal Fine Print: Cosigners, Collections, and Complex Debts

- Bankruptcy and Co-debtors on Student Loans: What Happens to the Cosigner?

- The Impact of Your Filing on a Cosigner

- Are Student Loans Unsecured Debt or Specialized Liabilities?

IV. Plan B: Alternatives if Discharge is Denied

- Total and Permanent Disability (TPD) Discharge vs. Bankruptcy

- How to Get Student Loans Out of Default Without a Lawyer

- Managing Collections and Stopping Garnishment Immediately

V. Frequently Asked Questions (FAQ)

VI. Conclusion: Navigating Your Path to Relief

- Next Steps for Your Fresh Start

Key Takeaways: What You Need to Know in 2026

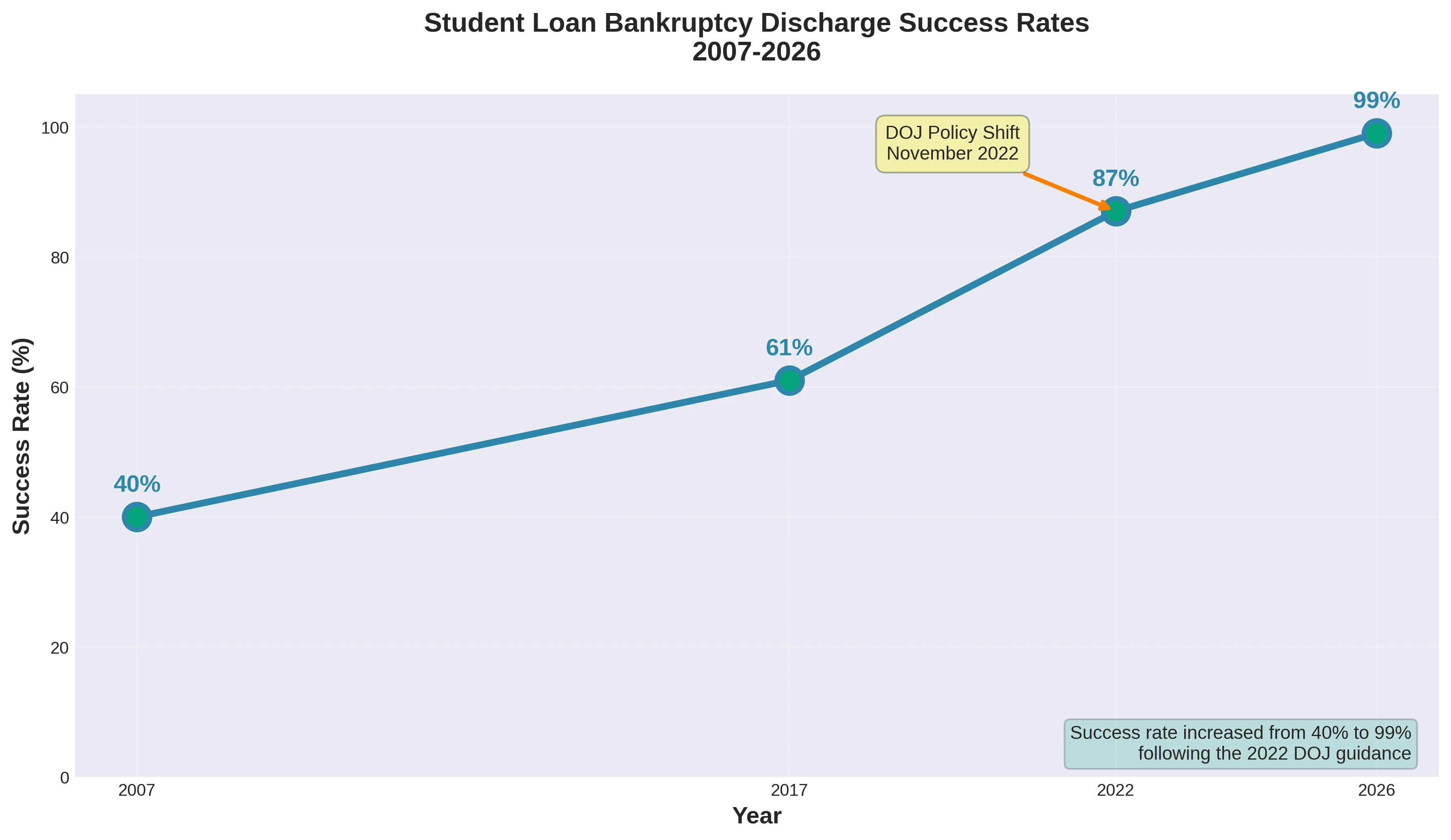

- A Massive Success Rate: As of 2026, the Department of Justice (DOJ) recommends a full or partial discharge in 99% of student loan bankruptcy cases that reach a judgment.

- Paperwork Over Trials: The new Attestation Review process allows many borrowers to qualify for discharge through a streamlined paperwork evaluation rather than a grueling courtroom trial.

- Strategic Protections: Filing for bankruptcy triggers an automatic stay, which stops aggressive collection tactics like student loan garnishment immediately.

- Cosigner Caution: Discharging your own debt does not automatically free a cosigner. In Chapter 7, lenders may still begin or continue collections against them.

- The TPD Alternative: If you have a disability expected to last at least 60 months, you may qualify for an administrative TPD discharge, which bypasses the bankruptcy courts entirely.

I. Introduction

If you’ve been told that your student debt is a “permanent” fixture in your financial life, you aren’t alone. For years, the prevailing wisdom was that these loans followed you forever, but as of early 2026, that landscape has shifted dramatically. Are student loans discharged in bankruptcy? The short answer is yes and more successfully than ever before.

Recent data from the Department of Justice (DOJ) highlights a surge in relief: in cases where a bankruptcy court issued a final judgment since the 2022 policy shift, the DOJ recommended a full or partial discharge in 99% of instances. This modern reality is a far cry from the old days of “mission impossible” legal battles.

Understanding the Success Rates: The Shift Since 2022

The current success is largely due to a landmark study published in The American Bankruptcy Law Journal, which looked at the impact of the November 2022 DOJ guidance. This study found that the success rate for borrowers seeking to discharge student loans surged to 87% following the new federal standards, a massive leap from just 40% in 2007 and 61% in 2017. This shift was driven by the government’s more objective framework for assessing hardship.

In the first 17 months following the November 2022 guidance (stretching into late 2024), there were 1,220 filings for student loan discharge. During just the first 10 months of that period, 632 adversary proceedings were filed, representing a significant increase in borrowers successfully navigating the system through a more streamlined, paperwork-based attestation process.

II. The Brunner Test and the New “Undue Hardship” Standards

For decades, the gatekeeper to debt relief was a strict legal hurdle known as the undue hardship test. While the core law hasn’t changed, the way the government looks at your financial struggle has.

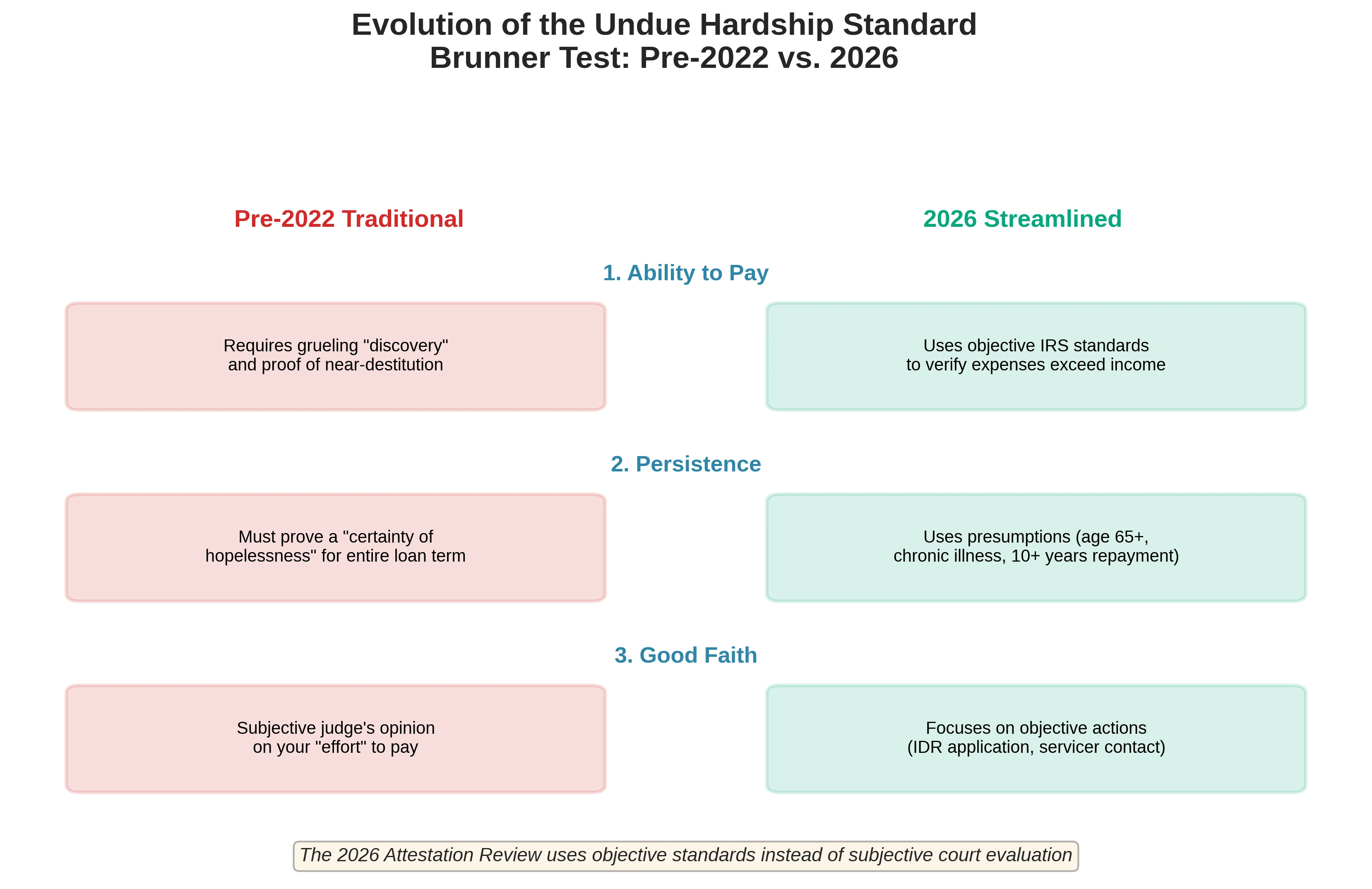

The standard still relies on the three-pronged Brunner Test:

- Ability to Pay: Can you maintain a “minimal standard of living” while paying the loans?

- Persistence: Is your financial situation likely to stay this way for a long time?

- Good Faith: Have you tried your best to manage the debt through repayment plans or contacting your servicer?

The 2026 difference is that the DOJ now uses a streamlined Attestation Review. Instead of an intimidating trial, federal borrowers can often complete a paperwork-based evaluation where the DOJ uses objective IRS standards to verify their financial hardship.

| Brunner Test Prong | Traditional Requirement (Pre-2022) | 2026 Streamlined Standard (Attestation) |

|---|---|---|

| 1. Ability to Pay | Requires grueling “discovery” and proof of near-destitution. | Uses objective IRS standards to verify if your current expenses exceed your income. |

| 2. Persistence | Must prove a “certainty of hopelessness” for the entire loan term. | Uses presumptions (e.g., being age 65+, chronic illness, or 10+ years in repayment) to assume persistence. |

| 3. Good Faith | Subjective judge’s opinion on your “effort” to pay. | Focuses on objective actions, such as applying for an IDR plan or communicating with your servicer. |

Table 1: Evolution of the Undue Hardship Standard.

Why student loans are not traditionally discharged and how it is changing

Many people wonder why student loans are not discharged in bankruptcy like credit cards or medical bills. Legally, they are classified under Section 523(a)(8) as specialized liabilities rather than standard unsecured debt. This means they require an extra step, a separate lawsuit called an adversary proceeding for student loans, to prove that keeping the debt would cause “undue hardship”.

However, the “hostile” nature of these proceedings is fading. The government now aims to identify cases where discharge is appropriate early in the process to reduce the burden on honest borrowers.

Proving undue hardship in court: Step-by-step

If you’re wondering how to prove undue hardship in court under the current 2026 guidelines, the process is now much more transparent:

- File your Bankruptcy Case: Whether it’s Chapter 7 or Chapter 13.

- Initiate an Adversary Proceeding: This is the formal “lawsuit within a bankruptcy” to address your student debt.

- Submit the Attestation Form: This is the most critical update. You’ll provide a detailed breakdown of your finances using a standardized form.

- DOJ Review: The DOJ and Department of Education review your paperwork. If you fit certain “presumptions” like being age 65+, having a chronic illness, or being in repayment for over 10 years, your case may be fast-tracked for a discharge recommendation.

| Presumption Category | 2026 Evidence Requirement |

|---|---|

| Age | Borrower is 65 years or older |

| Long-Term Repayment | Borrower has been in repayment for 10+ years |

| Disability | Long-term disability or chronic health condition |

| Unemployment | Extended unemployment or no completed degree |

Table 2: The 2026 “Fast-Track” Presumptions.

III. The Legal Fine Print: Cosigners, Collections, and Complex Debts

Understanding the 2026 reality of student loan discharge often requires looking beyond your own financial picture. Whether you are worried about the family member who signed the paperwork with you or confused about why these loans are treated differently than a credit card, these nuances are key to a successful bankruptcy strategy.

Bankruptcy and Co-debtors on Student Loans: What Happens to the Cosigner?

One of the biggest concerns for borrowers is what happens to co-debtors in bankruptcy. It is a common misconception that discharging your own obligation automatically frees your cosigner as well. In reality, the legal obligation is often tied to the individual, not just the loan itself.

The Impact of Your Filing on a Cosigner

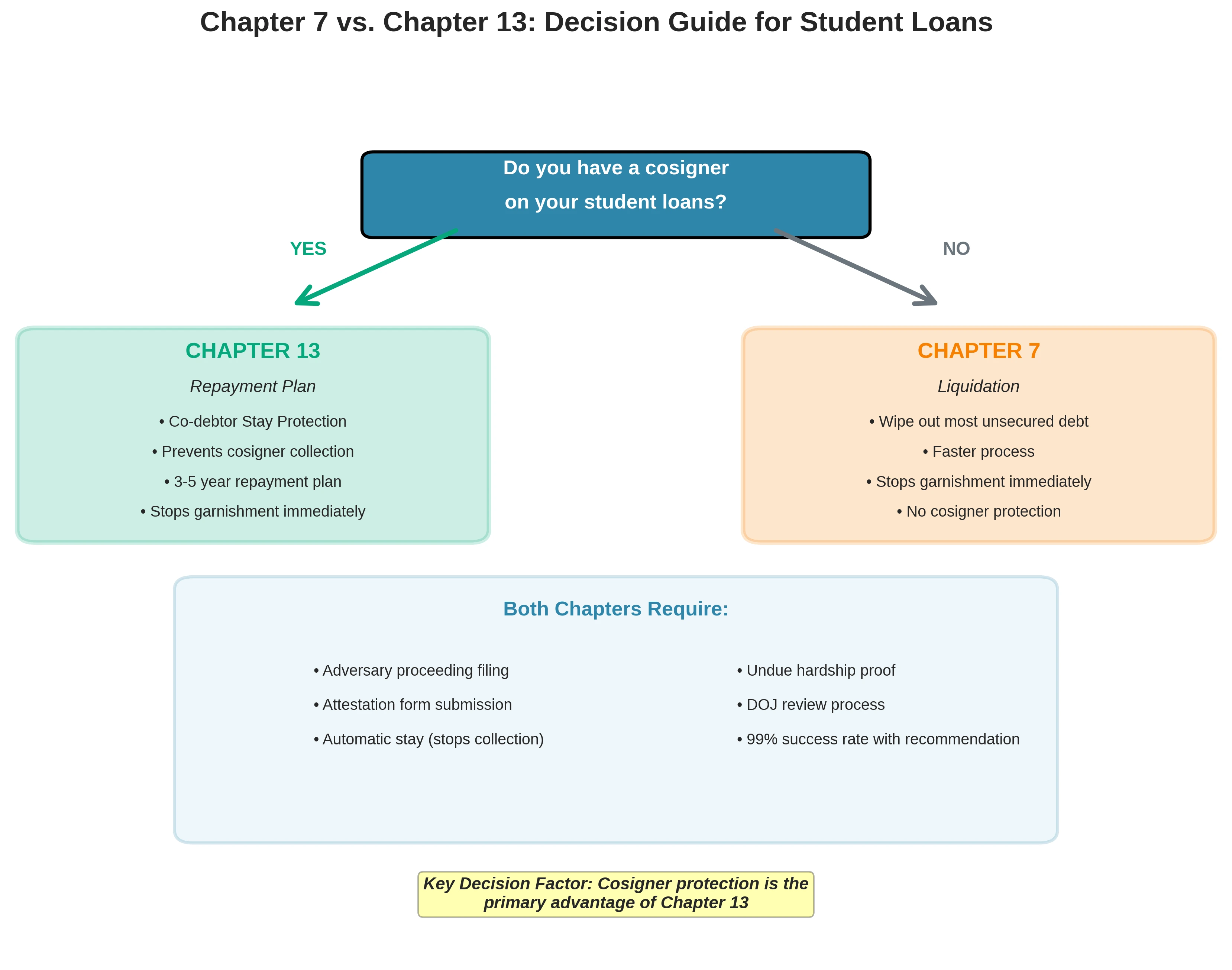

- Chapter 7 Risks: In a Chapter 7 “liquidation” bankruptcy, your cosigner receives no automatic protection. While your liability may be discharged, the lender can immediately pursue the cosigner for the full remaining balance, including through legal actions or wage garnishment.

- The Chapter 13 “Co-debtor Stay”: This is a critical advantage of Chapter 13. While your 3-to-5-year repayment plan is active, a co-debtor stay prevents creditors from contacting or collecting from your cosigner. This protection lasts as long as the case is active and in good standing.

- Independent Discharge: For a cosigner to be fully released, they must typically meet the undue hardship test based on their own unique financial circumstances, not yours.

| Feature | Chapter 7 (Liquidation) | Chapter 13 (Repayment) |

|---|---|---|

| Primary Goal | Wipe out most unsecured debt | Reorganize debt into a 3–5 year plan |

| Cosigner Status | No protection; lenders can collect | Protected by the Co-debtor Stay |

| Garnishment | Stops immediately via Automatic Stay | Stops immediately via Automatic Stay |

| Attestation | Required after filing lawsuit | Required after filing lawsuit |

Table 3: Chapter 7 vs. Chapter 13 for Student Loans.

Are Student Loans Unsecured Debt or Specialized Liabilities?

You might hear student loans described as unsecured debt, which is technically true because there is no collateral (like a house or car) backing the loan. However, the law treats them as specialized liabilities under Section 523(a)(8) of the Bankruptcy Code.

- Default Status: Unlike credit cards, student loans are “non-dischargeable” by default.

- The Adversary Requirement: To bridge the gap between “unsecured” and “discharged,” you must file a separate lawsuit known as an adversary proceeding for student loans.

- Exceptions to the Rule: Some private student loans that do not meet the strict definition of a “qualified education loan,” such as those exceeding the cost of attendance, may actually be treated as standard unsecured debt and discharged without a hardship review.

IV. Plan B: Alternatives if Discharge is Denied

While the success rates for bankruptcy discharge have climbed to nearly 99% under 2026 guidance, it is always wise to have a secondary strategy. If a judge determines you don’t meet the current “undue hardship” standards, several administrative paths can still provide the fresh start you need.

Total and Permanent Disability (TPD) Discharge vs. Bankruptcy

If your inability to work is due to a long-term medical condition, a Total and Permanent Disability (TPD) discharge might be a faster, less expensive alternative to the bankruptcy courts.

- The Primary Difference: Bankruptcy requires a legal “adversary proceeding” and a judge’s decision. TPD is an administrative process handled directly through the Department of Education.

- Definition of Disability: For TPD, you must show an impairment that has lasted (or is expected to last) for at least 60 continuous months or could result in death.

- Automatic Data Matches: As of 2026, if your disability is already recognized by the VA or Social Security Administration (SSA), your federal loans may be discharged automatically via a data match without you needing to file a separate application.

- Tax Considerations: While TPD discharges were historically taxable, federal law currently excludes these discharges from being considered income by the IRS, though you should verify your specific state’s rules.

| Factor | Bankruptcy (Undue Hardship) | TPD Discharge |

|---|---|---|

| Process Type | Judicial (Lawsuit required) | Administrative (Application) |

| Timeframe | Varies by court schedule | 60-month persistence required |

| Tax Status | Generally non-taxable | Tax-exempt through Dec 31, 2025 |

| Success Rate | 99% (with DOJ recommendation) | Automatic for VA/SSA recipients |

Table 4: TPD Discharge vs. Bankruptcy Discharge

How to Get Student Loans Out of Default Without a Lawyer

If you are facing the stress of collections but aren’t ready for bankruptcy, you can take immediate action to stabilize your credit. You don’t necessarily need a legal team to navigate these steps:

- Loan Rehabilitation: You can “rehabilitate” a defaulted federal loan by making nine on-time, voluntary monthly payments within a 10-month period.

- Loan Consolidation: This allows you to combine defaulted federal loans into a new Direct Consolidation Loan, which brings the debt back into “good standing” almost immediately after you agree to an income-driven repayment plan.

- Fresh Start Initiative: Check if your loans qualify for the latest federal “Fresh Start” programs, which have simplified the jump from default back to current status as of late 2025.

Managing Collections and Stopping Garnishment Immediately

The moment you file for bankruptcy, an “automatic stay” goes into effect, which is the most powerful tool to stop student loan garnishment instantly.

- The Automatic Stay: This legal injunction prevents creditors from taking your wages, seizing tax refunds, or even calling you while your case is being reviewed.

- Defending a Lawsuit: If you are being sued by a private lender, you may have a student loan lawsuit defense if the statute of limitations has passed or if the lender cannot prove they own the original debt.

- Cleaning Credit After Student Loan Default: Once your loans are either rehabilitated or discharged, you can dispute student loans on your credit report that show inaccurate “default” statuses to begin the process of rebuilding your financial reputation.

V. Frequently Asked Questions

Q. Will student loans go away after death?

A: Generally, federal student loans are discharged upon proof of the borrower’s death. For private loans, the outcome depends on the specific lender’s policy. However, in a bankruptcy context, debt that is not discharged may still be considered a liability of the estate.

Q. Are student loans considered a liability or standard debt?

A: In legal and financial terms, student loans are both a liability and a debt. Specifically, they are categorized under Section 523(a)(8) of the Bankruptcy Code as specialized liabilities, meaning they are “non-dischargeable” by default unless you prove they cause an undue hardship.

Q. Who handles student loans after bankruptcy?

A: Once a bankruptcy case is closed, if the loans were not fully discharged, they return to the original student loan servicer or the Department of Education. If a discharge was granted, the DOJ and Department of Education coordinate to update the National Student Loan Data System and notify the borrower that the balance is zero.

VI. Conclusion: Navigating Your Path to Relief

Entering 2026, the once-unmovable mountain of student debt has finally become manageable for those willing to take the legal path toward a fresh start. While student loans are technically specialized liabilities rather than standard unsecured debt, the administrative shifts at the Department of Justice have opened a “manageable gate” for federal borrowers.

With a 99% success rate for government-recommended discharges, the evidence is clear: the system is now designed to help, not hinder, the honest borrower. Whether you pursue a discharge through the Brunner Test’s updated framework, a TPD discharge due to a medical condition, or a strategic loan rehabilitation plan, you are no longer without options.

Next Steps for Your Fresh Start:

- Act Early: The automatic stay in bankruptcy stops aggressive collection efforts like student loan garnishment the moment you file.

- Use the Attestation: Don’t let the fear of a trial stop you. The new paperwork-based Attestation Review simplifies proving “undue hardship” using objective financial criteria.

- Check Your Eligibility: If you are over age 65, have a chronic disability, or have been in repayment for over a decade, you may fit the new presumptions for an easier discharge path.

- Monitor Your Credit: After your discharge or rehabilitation is complete, take active steps toward cleaning credit after student loan default by verifying that all accounts are reported as closed and paid.

The “myth of non-dischargeability” is officially a thing of the past. By understanding these 2026 rules and moving forward with a clear plan, you can finally reclaim your financial future from the weight of student debt.

Related Articles