Student Loan Forgiveness 2026: PSLF, SAVE Plan, and Status Updates

Key Terms in This Article

- 120 Qualifying Payments

- The number of monthly payments required under PSLF, made while working full-time for a qualifying employer and enrolled in an eligible repayment plan. These payments do not need to be consecutive.

- 501(c)(3) Organization

- A nonprofit organization exempt from federal income tax under Section 501(c)(3) of the Internal Revenue Code. These organizations qualify as PSLF employers, though new restrictions apply as of July 1, 2026.

- American Rescue Plan Act (ARPA)

- Federal legislation passed in 2021 that made student loan forgiveness tax-free. This tax exemption expired on December 31, 2025. Income-driven repayment forgiveness is generally taxable again at the federal level starting January 1, 2026, while programs like PSLF and Teacher Loan Forgiveness remain tax-free.

- Borrower Defense to Repayment

- A federal program that discharges loans for students whose schools misled them, made false promises about job placement or graduate outcomes, or closed while students were enrolled or shortly after withdrawal.

- Direct Loans

- Federal student loans made directly by the U.S. Department of Education. These are the only loan types eligible for PSLF, though other federal loans can be consolidated into Direct Loans to qualify.

- Employment Certification Form (ECF)

- The document borrowers submit to verify their employment with a qualifying PSLF employer and track progress toward the 120-payment requirement. Now processed through the PSLF Help Tool.

- FFEL (Federal Family Education Loan)

- Older federal student loans made by private lenders but guaranteed by the government. These loans are eligible for Teacher Loan Forgiveness but must be consolidated into Direct Loans to qualify for PSLF.

- Highly Qualified Teacher

- For Teacher Loan Forgiveness purposes, an educator who holds at least a bachelor's degree, has full state certification (not emergency or provisional), and meets state requirements for the subject and grade level taught.

- Income-Driven Repayment (IDR)

- A category of federal repayment plans that calculate monthly payments based on income and family size, with remaining balances forgiven after 20, 25, or 30 years of qualifying payments.

- Low-Income School

- An elementary or secondary school that serves students from low-income families and qualifies for funding under Title I of the Elementary and Secondary Education Act.

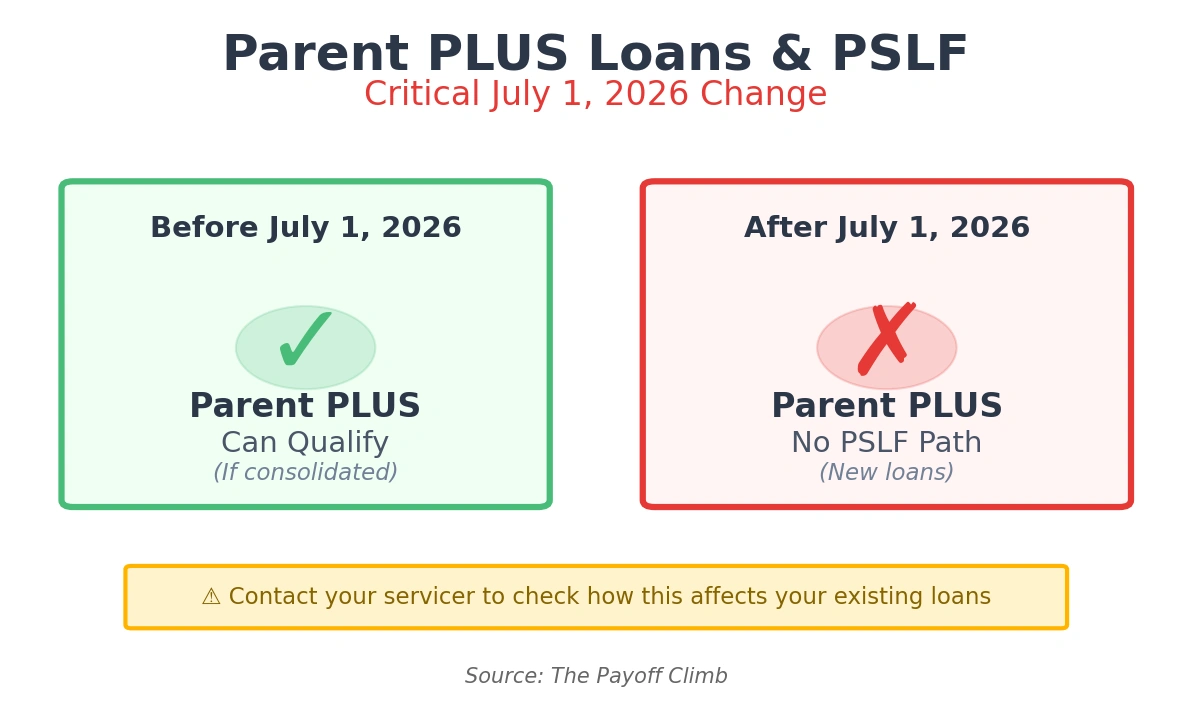

- Parent PLUS Loans

- Federal loans borrowed by parents to pay for a dependent student's education. For new Parent PLUS loans disbursed on or after July 1, 2026, there is no path to PSLF under current rules, while some existing Parent PLUS borrowers may retain PSLF eligibility if they consolidate and enroll in an eligible repayment plan before transition deadlines.

- Public Service Loan Forgiveness (PSLF)

- The federal program that forgives remaining Direct Loan balances after 120 qualifying monthly payments while working full-time for a qualifying government or nonprofit employer.

- Qualifying Employer

- For PSLF, a government organization at any level (federal, state, local, or tribal), 501(c)(3) nonprofit, or certain other nonprofit organizations providing qualifying public services. Effective July 1, 2026, employers determined to have a substantial illegal purpose by the Secretary of Education are excluded.

- SAVE Plan (Saving on a Valuable Education)

- An income-driven repayment plan proposed as REPAYE's replacement, currently subject to a settlement agreement announced December 9, 2025, awaiting court approval. Its future implementation remains uncertain.

- Teacher Loan Forgiveness (TLF)

- A federal program separate from PSLF that provides up to $17,500 in loan forgiveness for highly qualified teachers who work for five consecutive years in low-income schools.

Table of Contents

Key Takeaways

I. Introduction

II. The Current Landscape of Federal Forgiveness

-

Is student loan forgiveness still happening in 2026?

-

What student loans are eligible for forgiveness? The 2026 List

III. Student Loan Forgiveness by Career

-

How do I apply for student loan forgiveness as a teacher, nurse, or first responder?

-

What student loans qualify for PSLF?

IV. Managing the Application Process

-

How do I check the status of my student loan forgiveness application?

-

Forgiveness after 20 years: What are the income-driven rules?

V. Frequently Asked Questions

VI. Conclusion

Key Takeaways

• PSLF requirements remain 120 qualifying payments while working full-time for government or 501©(3) nonprofit employers, but new restrictions, effective July 1, 2026, exclude organizations with “substantial illegal purpose.”

• Parent PLUS loans lose PSLF eligibility if they are first disbursed on or after July 1, 2026.

• Income-driven repayment forgiveness became taxable on January 1, 2026, when the American Rescue Plan Act’s tax exemption expired. IDR forgiveness timelines vary by plan: 20 years under IBR (new borrowers) and PAYE, 25 years under IBR (old borrowers) and ICR, and 30 years under the new RAP plan expected July 2026.

• Teacher Loan Forgiveness offers up to $17,500 for highly qualified math, science, and special education teachers who complete five consecutive years at low-income schools, or up to $5,000 for other qualifying teachers.

• Submit Employment Certification Forms annually through the PSLF Help Tool at StudentAid.gov/pslf rather than waiting until you reach 120 payments, as retroactive verification becomes more difficult over time.

• Borrower Defense applications face court-ordered deadlines: January 28, 2026, for schools on the Exhibit C list (with automatic approval if missed) and April 15, 2026, for other post-class applications, though the Department requested extension through July 2027.

• Multiple IDR plans will be eliminated by July 1, 2028, borrowers on SAVE, PAYE, and ICR will be transitioned primarily to the new RAP plan, while some can remain in or move to IBR.

• Nurses and first responders should layer programs: pursue PSLF for Direct Loans while exploring National Health Service Corps loan repayment (up to $55,000), state shortage-area programs, and Perkins Loan cancellation for maximum benefit.

I. Introduction

If you are wondering whether student loan forgiveness is still happening in 2026, the short answer is yes, but with significant changes that took effect just weeks ago. On July 1, 2026, new Public Service Loan Forgiveness (PSLF) regulations narrowed which employers qualify for loan forgiveness while the tax-free status of income-driven repayment forgiveness ended on January 1, 2026. These shifts have left many borrowers asking: how do I check the status of my student loan forgiveness application? What student loans are eligible for PSLF? And perhaps most urgently for teachers, nurses, and first responders: how do I apply for student loan forgiveness in my career?

This guide cuts through the confusion surrounding the SAVE plan’s uncertain future and the shifting landscape of forgiveness after 20 years of payments. Whether you are a teacher seeking the $17,500 maximum forgiveness, a nurse exploring PSLF eligibility, or a first responder navigating qualifying employment requirements, you will find career-specific roadmaps and instructions for checking your application status with MOHELA, Nelnet, or Aidvantage.

The 2026 forgiveness landscape involves multiple pathways: Public Service Loan Forgiveness for government and nonprofit employees, Teacher Loan Forgiveness for educators at low-income schools, income-driven repayment plans that forgive remaining balances after 20 or 25 years, and borrower defense to repayment for students scammed by their schools. We will provide step-by-step guidance on applying for forgiveness as a teacher, nurse, first responder, mental health professional, social worker, healthcare worker, or any government or nonprofit employee.

This article addresses when student loans will be forgiven based on your specific situation, how recent Supreme Court decisions and executive actions have reshaped the programs, and whether private student loans are being forgiven. You will learn about the PSLF tracker, PSLF updates, employment certification requirements for nonprofit employees, and the tax consequences that now apply to forgiveness after 10 years of public service versus forgiveness after 20 years under income-driven plans.

II. The Current Landscape of Federal Forgiveness

Is student loan forgiveness still happening in 2026?

Yes, federal student loan forgiveness remains available in 2026, but recent regulatory changes have significantly altered who qualifies and how much borrowers may owe in taxes. Student loans were forgiven throughout 2025 under the same PSLF and Teacher Loan Forgiveness structures that continue today. However, new restrictions, taking effect July 1, 2026, will reduce the number of organizations that qualify as PSLF employers.

On October 30, 2025, the U.S. Department of Education published final regulations amending the definition of “qualifying employer” to exclude organizations that engage in unlawful activities constituting a “substantial illegal purpose,” including supporting terrorism or aiding illegal immigration. This change followed Executive Order 14235, signed by President Trump on March 7, 2025. The Department’s impact analysis estimates fewer than 10 employers will be affected annually, though legal experts warn the rule’s broad language could allow future administrations to exclude organizations based on ideological preferences. For borrowers currently pursuing PSLF, employer conduct before July 1, 2026, will not be considered, meaning past qualifying employment remains valid.

Beyond PSLF, income-driven repayment forgiveness continues after 20 or 25 years of qualifying payments, depending on which plan borrowers enrolled in and when they borrowed. However, the tax treatment changed dramatically on January 1, 2026. The American Rescue Plan Act of 2021 exempted all student loan forgiveness from federal taxation through December 31, 2025, but Congress did not extend this provision. Borrowers who receive IDR forgiveness in 2026 or later will owe federal income taxes on the forgiven amount. This tax liability does not apply to PSLF forgiveness, Teacher Loan Forgiveness, or Perkins Loan cancellation, only to income-driven repayment forgiveness.

Some federal guidance and legal documents suggest that, in situations where a borrower satisfied all forgiveness requirements in 2025 but the government did not finalize the discharge until 2026, the relief can sometimes be treated as having occurred in 2025 for federal tax purposes. Because this treatment is not automatic or universal, anyone in that position should confirm the tax year that will be used for their specific discharge.

What student loans are eligible for forgiveness? The 2026 List

Not all federal student loans qualify for every forgiveness program. For Public Service Loan Forgiveness, only Direct Loans are eligible, including Direct Subsidized Loans, Direct Unsubsidized Loans, and Direct Consolidation Loans. FFEL program loans and Perkins Loans do not qualify unless consolidated into a Direct Consolidation Loan.

Parent PLUS Loans underwent a major eligibility change effective July 1, 2026. Parent PLUS loans first disbursed on or after that date have no route into ICR or PSLF under current rules. However, some earlier Parent PLUS borrowers can keep access by consolidating and enrolling in eligible plans before the new cutoffs. Contacting your servicer is the best way to know how they will handle the payments you have already made.

For Teacher Loan Forgiveness, eligible loans include Direct Subsidized and Unsubsidized Loans, as well as FFEL program Stafford Loans. Direct PLUS Loans and FFEL PLUS Loans do not qualify. Borrowers should not have an outstanding Direct or FFEL loan balance as of October 1, 1998.

Private student loans are not eligible for any federal forgiveness programs. Getting relief usually means either pursuing bankruptcy or working out a settlement or cancellation directly with the private lender. On the other hand, Borrower Defense to Repayment discharges apply to Direct Loans and FFEL loans when schools engaged in fraud or misrepresentation. Under a court-ordered settlement, applications related to schools on the “Exhibit C list” are automatically approved if not decided by January 28, 2026. Other post-class applications have an April 15, 2026 deadline, though the Department requested extension through July 2027.

| Program | Best For | Years to Forgiveness | Federal Tax Status (Post-Jan 1, 2026) |

|---|---|---|---|

| PSLF | Gov & Nonprofit Employees | 10 Years (120 payments) | Tax-Free |

| Teacher Loan Forgiveness | Teachers in Low-Income Schools | 5 Consecutive Years | Tax-Free |

| IDR Forgiveness | General Borrowers | 20, 25, or 30 Years | Taxable |

| Borrower Defense | Students misled/scammed by schools | Varies (Application based) | Tax-Free |

Table 1: Federal Forgiveness Programs Comparison.

Now that you know which loans qualify, let’s explore how to apply based on your specific career.

III. Student Loan Forgiveness by Career

How do I apply for student loan forgiveness as a teacher, nurse, or first responder?

The application process differs significantly depending on which forgiveness program aligns with your career and loan type. Teachers have two primary pathways: Teacher Loan Forgiveness and Public Service Loan Forgiveness. Understanding which serves you better requires analyzing your specific employment situation.

For Teachers: If you work at a low-income school or educational service agency, you can pursue Teacher Loan Forgiveness by completing five consecutive years of full-time teaching. Verify your school’s eligibility using the Teacher Cancellation Low Income Directory. At least one qualifying year must occur after the 1997-98 academic year, and your loans must have been disbursed after October 1, 1998. To apply, submit the Teacher Loan Forgiveness Application with certification from your school’s chief administrative officer.

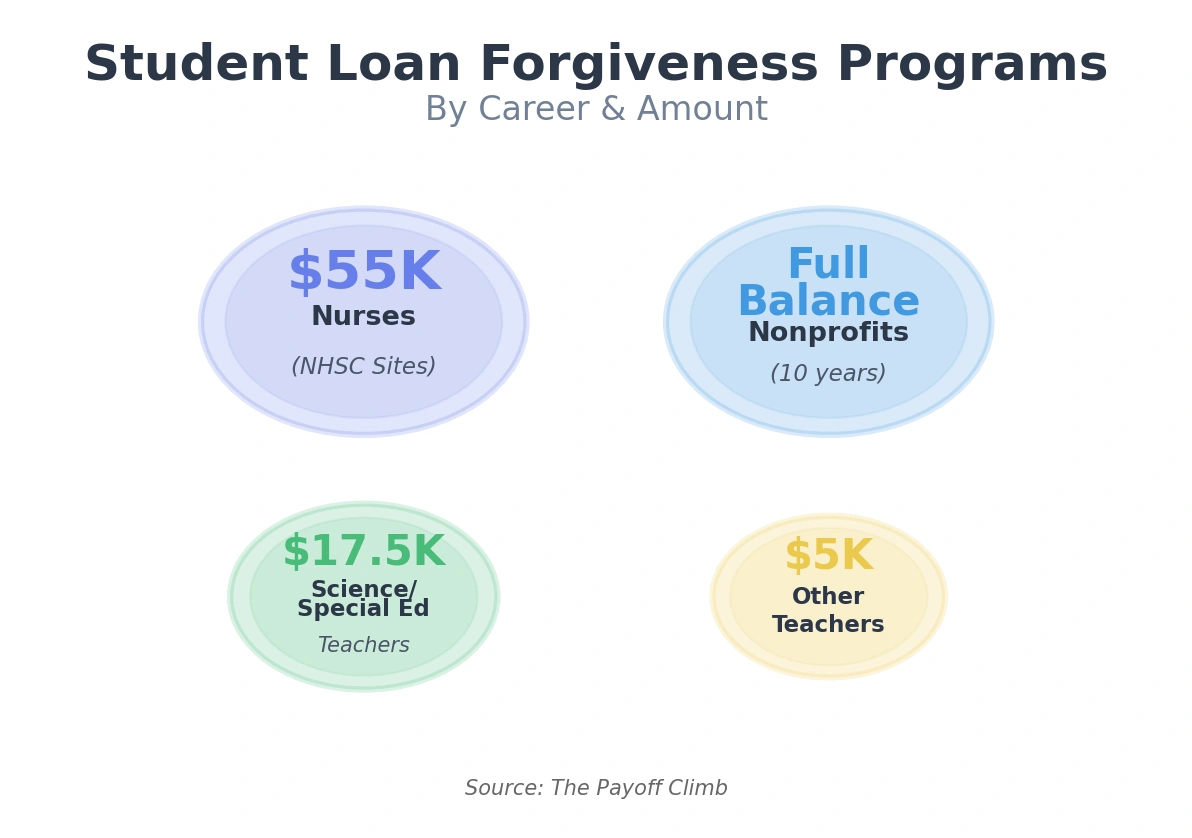

Highly qualified teachers, those holding at least a bachelor’s degree with full state certification meeting state requirements, qualify for up to $17,500 in forgiveness if teaching mathematics, science, or special education at the secondary level, and up to $5,000 for other full-time elementary and secondary teachers. You cannot receive both Teacher Loan Forgiveness and PSLF for the same service period, but you can receive Teacher Loan Forgiveness first, then continue toward PSLF for remaining balances.

If you work for a public school or a qualifying 501©(3) nonprofit school, you may benefit more from PSLF’s complete loan forgiveness after 120 payments. Use the PSLF Help Tool at StudentAid.gov/pslf to complete the Employment Certification Form. Submit these forms annually or whenever you change employers.

For Nurses: Public Service Loan Forgiveness represents the primary federal pathway for loan forgiveness. Nurses working for government hospitals, 501©(3) nonprofit hospitals, or qualifying nonprofit healthcare organizations can pursue PSLF by making 120 qualifying payments while employed full-time. The PSLF Help Tool determines whether your employer qualifies and generates the Employment Certification Form to submit at Federal Student Aid.

Beyond PSLF, nurses may qualify for the National Health Service Corps (NHSC) Loan Repayment Program, which provides up to $55,000 toward student loan repayment in exchange for two years of service at NHSC-approved sites in underserved areas. NHSC payments can count toward PSLF if you are pursuing both programs simultaneously. State-specific programs, such as Minnesota’s Mental Health Professionals Loan Repayment Assistance, offer additional support. You should always verify availability through your state’s health department or higher education agency.

For First Responders: Police officers, firefighters, and paramedics employed by government agencies qualify for PSLF following the same process as other government employees. Municipal fire departments, police departments, and emergency medical services automatically qualify as PSLF employers (subject to the July 1, 2026, substantial illegal purpose exclusions, though these rarely apply to traditional public safety agencies). First responders with eligible Perkins Loans may qualify for up to 100% cancellation over five years, depending on their specific role and service category.

What student loans qualify for PSLF?

Only William D. Ford Federal Direct Loan Program loans, commonly called Direct Loans, are eligible for Public Service Loan Forgiveness. This includes Direct Subsidized Loans, Direct Unsubsidized Loans, Direct PLUS Loans borrowed by graduate or professional students (not Parent PLUS Loans as of July 1, 2026), and Direct Consolidation Loans.

Federal Family Education Loans (FFEL) and Federal Perkins Loans must be consolidated into a Direct Consolidation Loan to qualify for PSLF. Parent PLUS Loans, borrowed by parents on behalf of dependent undergraduates, face tighter rules beginning July 1, 2026. New Parent PLUS loans disbursed on or after that date do not have a PSLF path, but some parents with older Parent PLUS loans can still qualify if they consolidate before the deadline and choose an eligible repayment option. Anyone in this situation should ask their servicer or Federal Student Aid how their past payments are being counted.

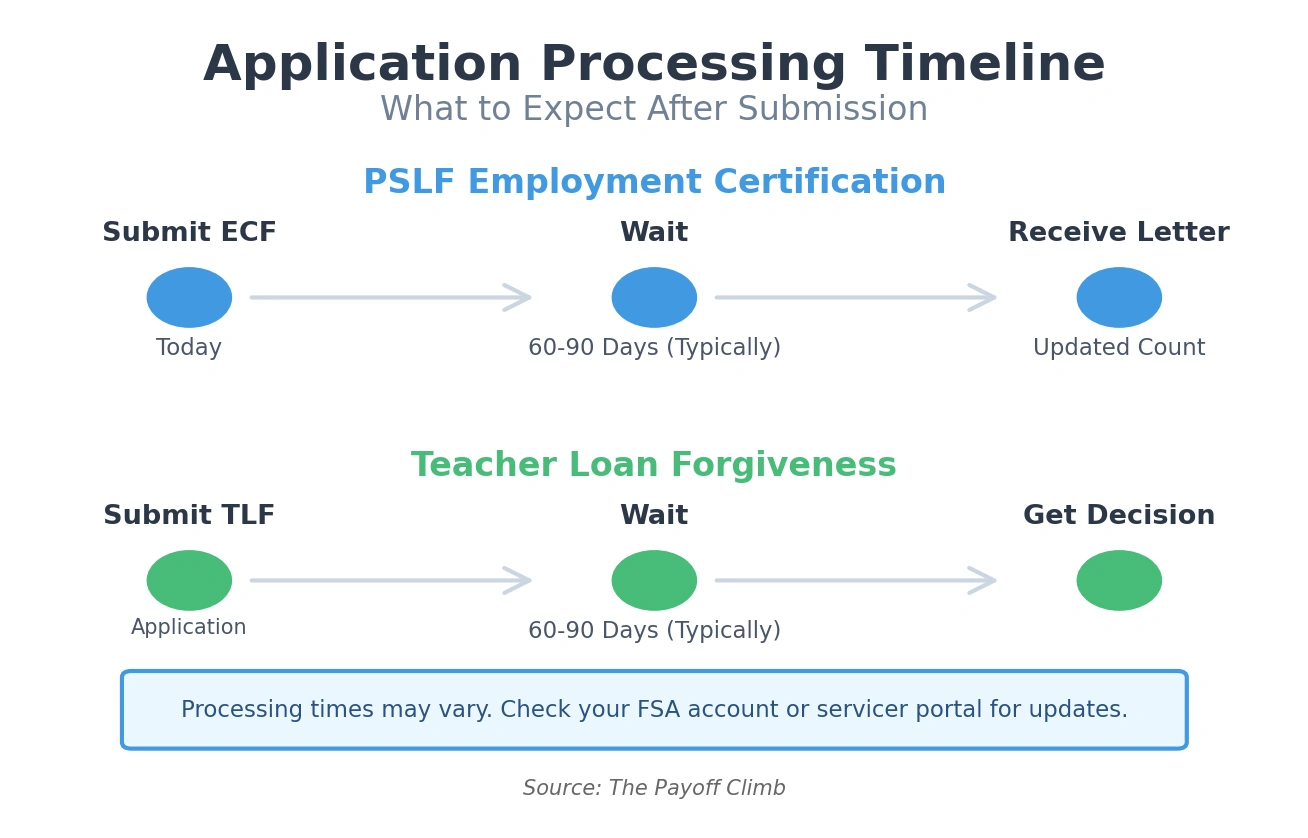

PSLF requires payments be made under Income-Driven Repayment plans or the 10-Year Standard Repayment Plan. The 120 qualifying payments do not need to be consecutive. You can leave and return to public service employment, resuming where you left off. However, you must be working for a qualifying employer when you submit your PSLF application after making your 120th payment. To verify your loans’ eligibility, use the PSLF Help Tool. Your official count of qualifying PSLF payments now appears in your Federal Student Aid online account.

IV. Managing the Application Process

How do I check the status of my student loan forgiveness application?

Checking your forgiveness application status depends on which program you are pursuing and which servicer manages your loans. For Public Service Loan Forgiveness, MOHELA (Missouri Higher Education Loan Authority) used to serve as the exclusive servicer processing all PSLF applications but since 2024, PSFL is directly managed by Federal Student Aid.

To check PSLF progress, log into your Federal Student Aid account and navigate to the PSLF payments on the dashboard. If you have submitted an Employment Certification Form within the last 90 days, processing typically takes about 60 to 90 days, though timelines can vary. Once processed, you will receive a letter detailing approved payments and updated progress. If you disagree with the payment counts, you can submit a PSFL Reconsideration Request online. It is in your best interest to submit this request within 60 days. For Teacher Loan Forgiveness, check your servicer account (Aidvantage, MOHELA, or EdFinancial). Applications take 60 to 90 days to process after submission.

For income-driven repayment forgiveness, the Department of Education is supposed to automatically grant IDR forgiveness once you reach the required number of qualifying months while on a qualifying plan, but processing can take time and may require that you are currently on an eligible plan. Review your payment history at least once a year on your servicer’s site and StudentAid.gov, keep your own records, and promptly file a dispute or reconsideration request if qualifying months appear to be missing or miscounted.

For Borrower Defense to Repayment, check status at Student Aid. If your application involves an Exhibit C school, the Department of Education must issue a decision by January 28, 2026, or it is automatically approved. All other post‑class applications must receive a decision by April 15, 2026.

| Application Category | Decision Deadline | Result if Deadline is Missed |

|---|---|---|

| Exhibit C Schools | Jan 28, 2026 | Automatic Approval of discharge |

| Other Post-Class Apps | April 15, 2026 | Pending (Dept. requested July 2027 extension) |

| New Applications | Varies | Individual review by Federal Student Aid |

Table 2: Critical 2026 Borrower Defense Deadlines.

For Total and Permanent Disability discharges, check status at Federal Student Aid. In March 2025, the Department of Education transferred TPD discharges from Nelnet to FSA. Processing typically takes about 60 to 90 days after FSA’s TPD unit receives all required documentation, but timelines can vary

Forgiveness after 20 years: What are the income-driven rules?

Income-driven repayment plans offer loan forgiveness after borrowers make qualifying payments for 20 to 30 years depending on their plan and when they borrowed. Understanding the timelines and tax consequences is critical, especially given the dramatic tax changes that took effect January 1, 2026.

The Income-Based Repayment (IBR) plan forgives loans after 20 years for borrowers who took out their first federal loan on or after July 1, 2014 (“new borrowers”), and after 25 years for those who borrowed before that date. This five-year difference significantly impacts lifetime repayment amounts. IBR forgiveness is achieved by making qualifying payments under a qualifying plan, even $0 payments when income is low enough. Most deferments and forbearances don’t count toward the payment requirement.

Pay As You Earn (PAYE) forgives remaining balances after 20 years regardless of when borrowers took out their first loans. Income-Contingent Repayment (ICR) requires 25 years of payments. Both PAYE and ICR will be eliminated by July 1, 2028.

The Revised Affordable Payment (RAP) plan, expected to launch around July 2026, extends forgiveness to 30 years, the longest timeline. Borrowers with loans disbursed before July 1, 2026, can maintain existing Standard, Extended, or IBR plans, but those on ICR, PAYE, or SAVE must transition to RAP or standard tiered by July 1, 2028, unless they qualify for IBR.

The tax consequences changed drastically on January 1, 2026. Forgiveness received on or after this date is treated as taxable income. If you receive $50,000 in forgiveness in the 22% federal tax bracket, you will owe approximately $11,000 in federal income taxes, plus state income tax. The Department of Education has indicated in some guidance and legal filings that when borrowers met forgiveness criteria in 2025 but processing extended into 2026, it may treat forgiveness as occurring in 2025 for tax purposes; borrowers should confirm how this applies in their specific situation.

Public Service Loan Forgiveness remains entirely tax-free regardless of when forgiveness occurs, as do Teacher Loan Forgiveness and Perkins Loan cancellation. Only income-driven repayment forgiveness after 20, 25, or 30 years is now taxable, creating a significant advantage for public service workers who can pursue PSLF’s 10-year pathway instead.

| IDR Plan | Forgiveness Timeline | Borrower Eligibility | Status in 2026 |

|---|---|---|---|

| PAYE | 20 Years | All eligible borrowers | Sunset July 2028 |

| New IBR | 20 Years | First borrowed on/after July 1, 2014 | Active |

| Old IBR | 25 Years | First borrowed before July 1, 2014 | Active |

| ICR | 25 Years | All eligible borrowers | Sunset July 2028 |

| RAP | 30 Years | New & transitioned borrowers | Launch July 2026 |

Table 3: Income-Driven Repayment (IDR) Timelines

V. Frequently Asked Questions

Q: How do I check the status of my student loan forgiveness application?

A: For PSLF applications, log into your FSA account to view your qualifying payment count and pending Employment Certification Forms while Teacher Loan Forgiveness applications should check through your servicer. Income-driven repayment forgiveness should process automatically when you reach your plan’s timeline.

Q: How do I apply for student loan forgiveness if I was scammed by my school?

A: Submit a Borrower Defense to Repayment application through the portal at studentaid.gov and document how your school misled you about job placement, graduate outcomes, or program details. Applications for schools on the “Exhibit C list” must receive decisions by January 28, 2026, and are automatically approved if the Department of Education misses this deadline. Post-class applications not involving Exhibit C schools have an April 15, 2026 decision deadline, though the Department requested extension through July 2027 in January 2026.

Q: Which student loans are forgiven after 10 years?

A: Only Direct Loans, including Direct Subsidized, Direct Unsubsidized, Direct PLUS (for graduate students), and Direct Consolidation Loans, are forgiven after 10 years through Public Service Loan Forgiveness. It requires 120 qualifying monthly payments while working full-time for qualifying government or 501©(3) nonprofit employers. Parent PLUS Loans disbursed on or after July 1, 2026 no longer qualify for PSLF. Some existing Parent PLUS borrowers may still qualify for PSFL if they consolidate and enroll in an eligible plan before the transition deadlines. FFEL and Perkins Loans must be consolidated into Direct Consolidation Loans to qualify.

Q: How do I apply for student loan forgiveness for mental health professionals?

A: Mental health professionals have multiple pathways. One of them is PSLF if you work for the government or 501©(3) nonprofit mental health facilities. Alternatively, Minnesota offers loan repayment assistance providing $11,000 annually for social workers, therapists, and counselors, or $29,000 annually for psychologists serving rural or urban shortage areas. Licensed clinical social workers can access National Health Service Corps loan repayment up to $55,000 for two years of service at NHSC-approved sites in underserved areas.

Q: Are student loans forgiven after 25 years?

A: Yes, but with significant tax consequences starting January 1, 2026. Income-Based Repayment forgives loans after 25 years for borrowers who borrowed before July 1, 2014. Income-Contingent Repayment (ICR) requires 25 years of payments (though ICR will be eliminated by July 1, 2028). The American Rescue Plan Act’s tax exemption expired December 31, 2025, making income‑driven repayment forgiveness generally taxable at the federal level. Borrowers will then receive Form 1099-C reporting canceled debt as income. New borrowers under IBR (first loan on or after July 1, 2014) and PAYE enrollees receive forgiveness after 20 years instead of 25. PSLF, Teacher Loan Forgiveness, and Perkins cancellation remain tax‑free.

VI. Conclusion

The student loan forgiveness landscape in 2026 demands immediate action. If you work in public service, submit your Employment Certification Form through the PSLF Help Tool today. If you wait to submit an Employment Certification until you have made 120 payments, retroactive employment verification becomes more difficult as employers close or change record-keeping systems. Teachers at low-income schools should calculate whether Teacher Loan Forgiveness’s $5,000 to $17,500 immediate benefit outweighs pursuing PSLF’s complete forgiveness after 120 payments.

For borrowers pursuing income-driven repayment forgiveness, the January 1, 2026 tax change transforms forgiveness into a taxable event. If you are within five years of reaching your 20, 25, or 30-year threshold, begin setting aside 20 to 30% of your expected forgiveness amount for tax liability. High-balance borrowers expecting six-figure forgiveness should consult a tax professional about minimizing impact through timing strategies or IRS installment agreements.

First responders and nurses should layer state programs like Minnesota’s Mental Health Professional Loan Repayment Assistance and the National Health Service Corps alongside PSLF for maximum benefit. The shifting regulatory environment, including the SAVE plan settlement and pending borrower defense extensions, requires vigilance.

Be proactive. Take control of your student loan debt. Check your application status today, submit pending Employment Certification Forms promptly, and mark your calendar for annual recertification deadlines. When we treat forgiveness with due diligence, we are far more likely to receive it smoothly and without unnecessary delays.

Related Articles