The "Servicer Directory": Discovery, Tracking, & Consolidation

Key Terms in This Article

- Direct Consolidation Loan

- A federal loan that combines multiple federal education loans into one, resulting in a single monthly payment and a fixed interest rate.

- Loan Servicer

- A company that handles the billing and other services on your federal student loan on behalf of the Department of Education.

- Master Promissory Note (MPN)

- The legal document in which you promise to repay your loan and any accrued interest and fees to the U.S. Department of Education.

- Public Service Loan Forgiveness (PSLF)

- A program that forgives the remaining balance on your Direct Loans after you have made 120 qualifying monthly payments under a qualifying repayment plan while working full-time for a qualifying employer.

- Repayment Assistance Plan (RAP)

- The primary income-driven repayment plan introduced by OBBBA in 2025, designed to simplify and replace older IDR plans.

- Weighted Average Interest Rate

- The interest rate on a consolidation loan, calculated by taking the weighted average of the interest rates on the loans being consolidated, rounded up to the nearest one-eighth of one percent.

Table of Contents

Key Takeaways

I. Introduction

II. Tracking Multiple Student Loans: A Step-by-Step Guide

III. Navient, MOHELA, Nelnet: Tracking a Servicer Transfer

- Table 1: Comparison of Major 2026 Servicers

IV. The Consolidation Roadmap

- How do I consolidate federal student loans in 2026?

- Consolidating for PSLF: What you need to know

- Consolidation vs. Refinancing: Choosing the Right Path

- Table 3: Key Differences between Federal Consolidation vs. Private Refinancing

V. Special Situations: School Closures and Taxes

VI. Frequently Asked Questions

VII. Conclusion

Key Takeaways

- Identify Your Servicer First: Use your dashboard at StudentAid or call 1-800-433-3243 to determine which of the four primary federal servicers, Aidvantage, Edfinancial, MOHELA, or Nelnet, holds your debt.

- Locate Your Identifiers: Your unique Student Loan Account Number and Loan Sequence Number are found within the “My Aid” section of your federal profile. These identifiers are essential for any servicer transfer or consolidation application.

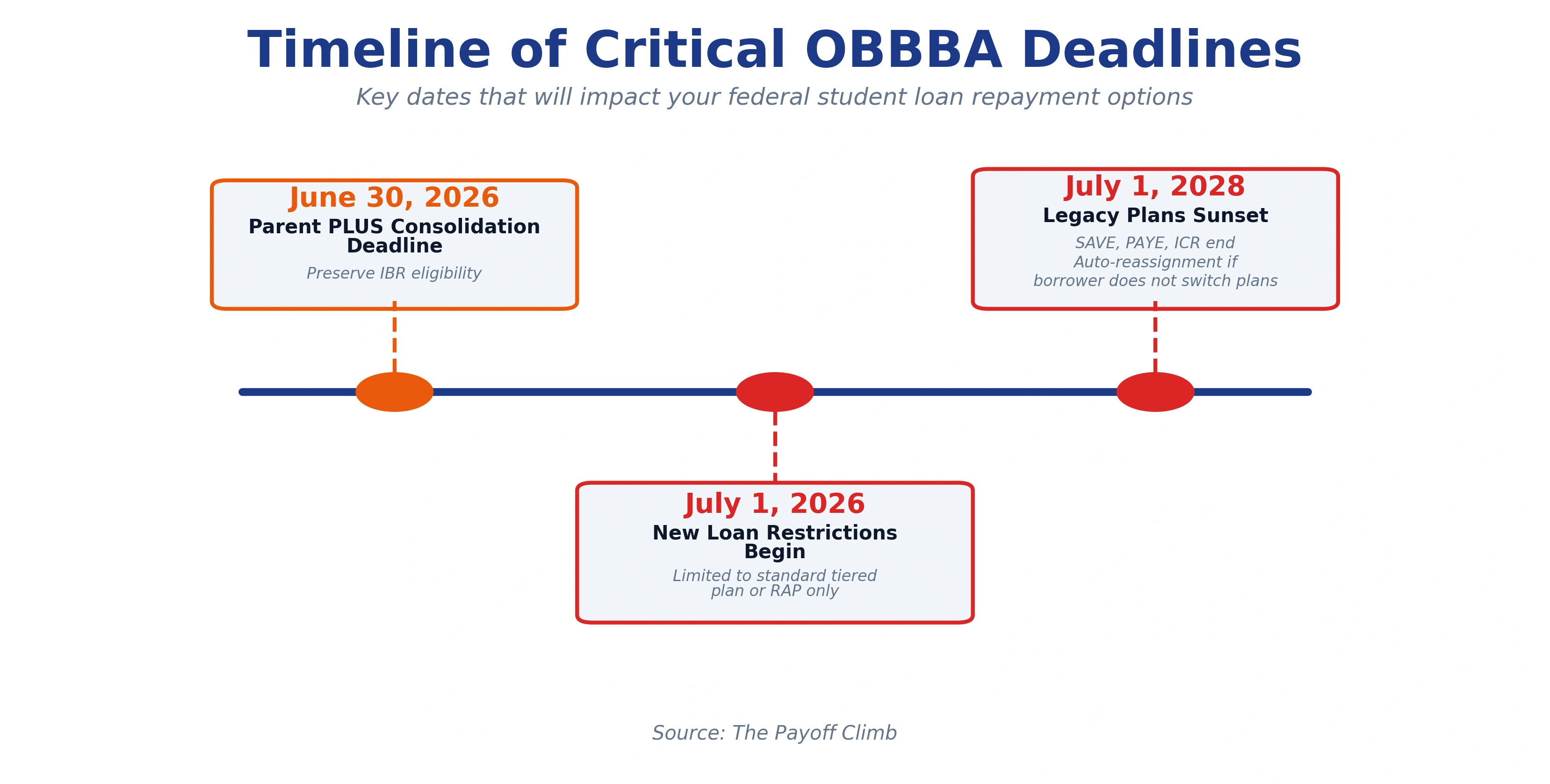

- Consolidation Timeline: To qualify for the maximum benefits under the 2026 One Big Beautiful Bill Act (OBBBA) and preserve Public Service Loan Forgiveness (PSLF) progress, FFEL and Perkins loan holders should consolidate into the Direct Loan program by the June 30, 2026, transition deadline.

- Transfer Awareness: If your loan was moved (e.g., from Navient to Aidvantage), your original promissory note remains legally binding, but you must register a new online account with the receiving servicer to maintain payment history visibility.

- Federal vs. Private: Consolidation keeps your loans within the federal system, preserving death and disability discharge protections whereas refinancing into a private loan permanently removes all federal subsidy and forgiveness eligibility.

I. Introduction

In 2026, the federal student loan portfolio totals about $1.7 trillion in outstanding federal debt owed by roughly 43–45 million borrowers, according to recent federal data and nonpartisan summaries. Beginning July 1, 2026, borrowers who take out new federal loans will see a streamlined repayment system in which new borrowing generally leads to two primary options: a fixed “tiered standard” repayment plan and a single income‑driven Repayment Assistance Plan (RAP) while most existing borrowers may remain in or transition among legacy plans under specific grandfathering rules and deadlines.

For federal loans first disbursed on or after July 1, 2026, borrowers will typically start in the standard plan (with a term of roughly 10 to 25 years depending on balance) unless they opt into RAP, the only income‑driven option for those new loans. Borrowers who do not take on any new loans after July 1, 2026 can generally stay in existing plans, such as SAVE, Income‑Based Repayment (IBR), Graduated, Extended, Standard, or switch to RAP by July 1, 2028. On July 1, 2028, SAVE, PAYE, and ICR plans will sunset and borrowers who do not switch plans will be automatically reassigned under the new rules, with many moved into RAP. All these new deadlines and transition rules make it critical to review your loan types and repayment options before those grandfathering windows close.

Carefully managing your loans means knowing exactly which company services your accounts. It is important to monitor changes as Federal Student Aid reallocates portfolios among different providers as, for instance, some servicers exit the federal program (e.g., Navient to Aidvantage in 2021-2022). This guide is designed to help you identify your current servicer, locate key account identifiers, and choose or adjust a consolidation and repayment strategy that fits the rules taking effect for loans disbursed and consolidated on or after July 1, 2026.

How to find your student loan servicer and account numbers

The first question most borrowers ask is: how do I know who my student loan servicer is? Identifying your servicer is the prerequisite for every other action, from checking your balance to applying for forgiveness. A loan servicer is the private company assigned by the Department of Education to handle the monthly billing and administrative tasks for your federal loans.

The easiest way to find your student loans servicer is to log into your dashboard at StudentAid. Once logged in, navigate to the “My Aid” section. Here, you will see a “My Loan Servicers” list which provides the contact information for every company holding your federal debt. If you cannot access the website, you can contact the Federal Student Aid (FSA) Information Center at 1-800-4-FED-AID.

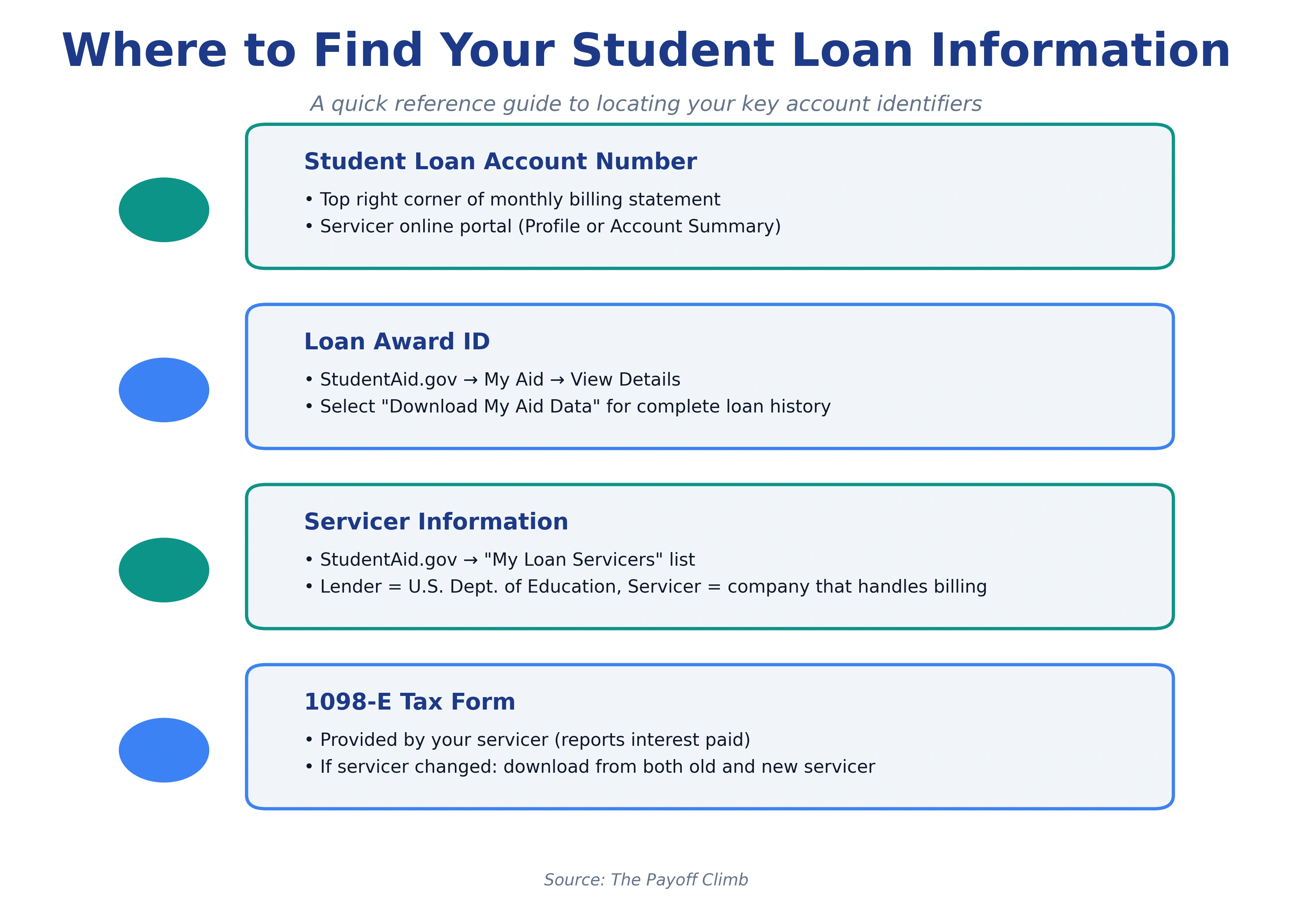

For those looking for their student loan account number, this information is typically located in the top right-hand corner of your monthly billing statement or within your servicer’s secure online portal. Each servicer assigns a unique account ID to your profile. If you have loans with multiple providers, you will have multiple account numbers to track.

For advanced management, you may want to see the unique identifier assigned to each loan (e.g., Loan Award ID). This makes it easier to distinguish between different loans (such as a subsidized or unsubsidized loan) taken out during the same academic year.

Follow these steps to download detailed identifiers for each of your loans:

- Go to Student Aid

- Log in to your account.

- On the dashboard, click on “View Details” under the “My Aid” section.

- Select “Download My Aid Data.”

This will generate a text file containing every technical detail of your loan history, including the Loan Award ID, disbursement date, and other fields for each disbursement.

II. Tracking Multiple Student Loans: A Step-by-Step Guide

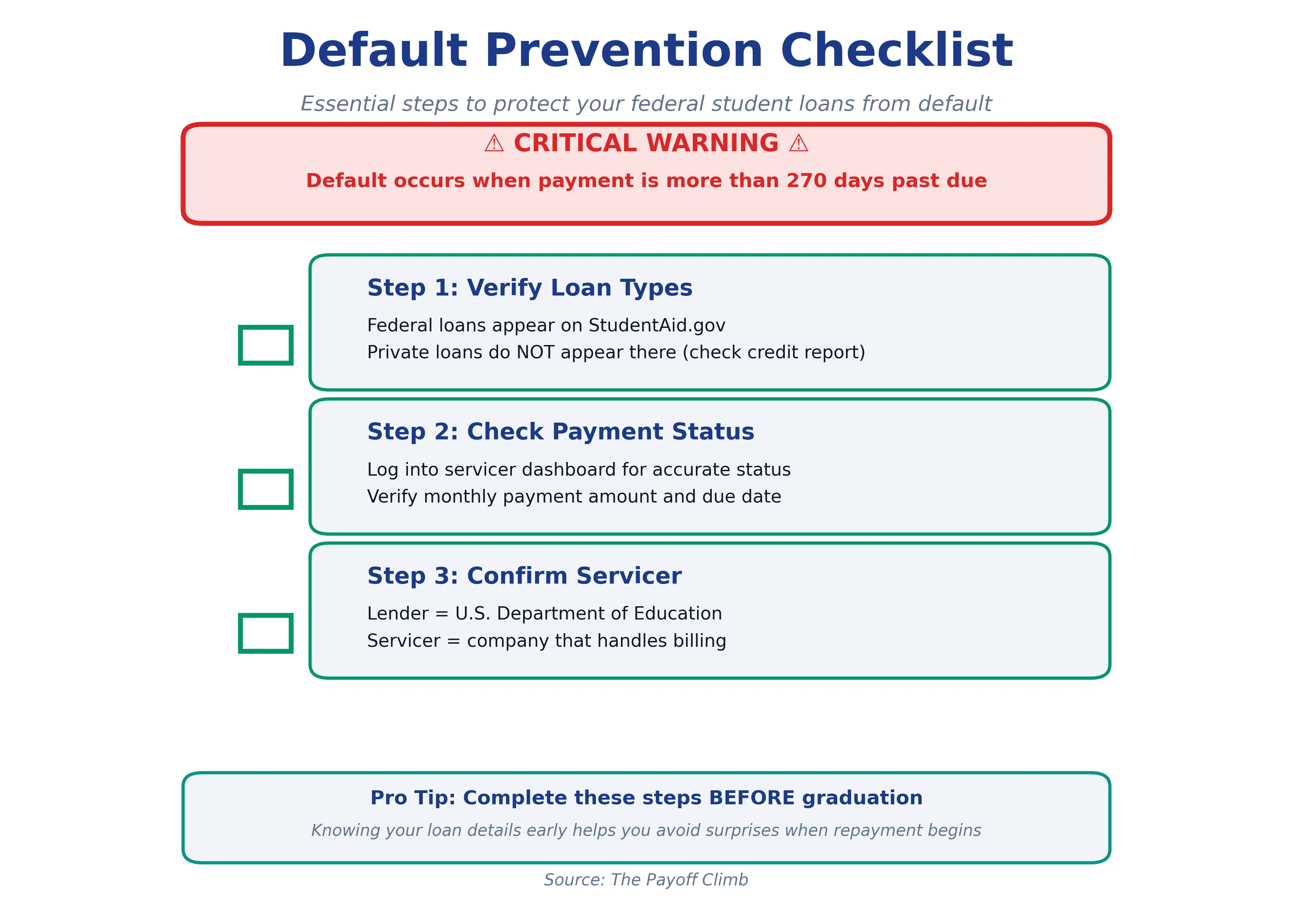

Many borrowers hold multiple loans, so keeping a clear record of these accounts is vital to avoiding default. For most federal loans, default occurs when a payment is more than 270 days past due. Before graduation, consider following these steps to ensure you will be ready when repayment starts:

- Verify Loan Types: It is critical to know if you have federal and/or private student loans. Federal loans will appear on StudentAid while private loans generally do not. Private loans are held by banks or credit unions and do not qualify for federal repayment programs or forgiveness.

- Check Payment Status: To find out your student loan payment status and monthly payment, your servicer’s dashboard is the most accurate source.

- Confirm Student Loan Servicer: If you are unsure which company holds your student loans or where student loans are held, remember that the “lender” for all modern federal loans is the U.S. Department of Education, but the “servicer” is the company you actually pay.

III. Navient, MOHELA, Nelnet: Tracking a Servicer Transfer

The student loan landscape is undergoing major servicing contract changes, leading to frequent student loan servicer changes over the last several years. A major recent change for many borrowers was the transfer of federal loans from Navient to Aidvantage in late 2021 and early 2022, which some borrowers are still untangling in 2026.

If you were part of recent servicer transfer cycles involving Navient, Aidvantage, MOHELA, or Nelnet, here is how to track servicer transfer progress:

- The 7-10 Day Lag: When a transfer occurs, it can take about 7 to 10 business days, sometimes longer, for your information to fully populate in the new servicer’s system.

- The Legal Anchor: Even during a servicer switch, you are still legally bound to your student loan promissory note. You can usually request a student loan promissory note copy from your new servicer or find the digital version under “My Documents” on StudentAid.

- Payment History: To check your student loan payment history, go to StudentAid and navigate to the “Dashboard” and select “View Details” on your individual loans.

| Feature | Aidvantage | MOHELA | Nelnet | Edfinancial |

|---|---|---|---|---|

| Primary Focus | General Servicing for federal Direct Loans. | General Servicing for federal Direct Loans. | General Servicing of federal loans. | General Servicing of federal loans. |

| 2026 Transition | Services many former Navient accounts. | No longer the dedicated PSLF servicer. | Services consolidated and Direct portfolios. | Services former Granite State and other portfolios. |

| Account Access | Aidvantage | MOHELA | Nelnet | Edfinancial |

Table 1: Comparison of Major 2026 Servicers

Once you know which servicer holds your account, you need to understand how to reach them and navigate their systems. Here is a quick reference guide to the four major federal student loan servicers in 2026.

| Servicer | Best Time to Call (Local Time) | Pro-Tip for 2026 |

|---|---|---|

| MOHELA | 7:00 AM – 7:30 AM CT | For general account questions, call early on Tuesday or Wednesday. Note: MOHELA is no longer the PSLF servicer. PSLF is now managed by StudentAid.gov directly. |

| Nelnet | 8:00 AM – 8:30 AM ET | Call early in the week (Tuesday–Wednesday) for shorter wait times. Nelnet’s 2026 hours: Mon 8 AM – 11 PM ET; Tue–Fri 8 AM – 8 PM ET; Sat 10 AM – 2 PM ET. |

| Aidvantage | 8:00 AM – 9:00 AM ET | Log into the portal first and try AVA (the chatbot). It can resolve most general questions or bridge you to a live agent, often bypassing the standard phone queue. |

| Edfinancial | 8:00 AM – 8:30 AM ET | Avoid calling on Mondays if possible, as volume is highest due to the weekend backlog. Utilize their extended Monday hours (until 11 PM ET) only as a last resort. |

Table 2: Servicer Call Strategy and Pro-Tips

IV. The Consolidation Roadmap

How do I consolidate federal student loans in 2026?

Given OBBBA’s new deadlines, borrowers, especially those with Parent PLUS loans, should consider consolidating by June 30, 2026 to preserve eligibility for certain grandfathered plans such as IBR. Borrowers who take out or consolidate loans on or after July 1, 2026 will generally be limited to the standard tiered plan or RAP. A Direct Consolidation Loan allows you to combine multiple federal education loans into one loan with a single monthly payment.

The process for federal student loan consolidation involves a single student loan consolidation application whose status you can track online. To apply, you must complete the direct consolidation loan application and sign a new promissory note.

Consolidating for PSLF: What you need to know

For those looking at how to consolidate for PSLF, the stakes are high. If you have older Federal Family Education Loans (FFEL), you must consolidate them into a Direct Consolidation Loan to make them eligible for Public Service Loan Forgiveness.

When considering FFEL vs Direct Loan Consolidation, remember that:

- Consolidating student loans for PSLF used to reset your payment count to zero, but under the weighted average rule implemented in September 2024, you now retain a weighted average of your existing qualifying payments when you consolidate.

- Student loan consolidation application status: Once the application is submitted, you can view its progress through the “My Activity” section of your StudentAid account.

Consolidation vs. Refinancing: Choosing the Right Path

It is vital to distinguish between student loan consolidation vs refinancing. While the terms are often used interchangeably, they have vastly different impacts on your financial safety net.

Choosing federal vs private consolidation depends on your goals. If you value the safety and protections of federal repayments plans, stick with federal consolidation.

| Feature | Federal Consolidation | Private Refinancing |

|---|---|---|

| Lender | U.S. Department of Education | Private Bank/Lender |

| Interest Rate | Weighted average of current loans | Based on credit score |

| Forgiveness | Eligible for grandfathered plans and PSLF | Ineligible for all federal forgiveness |

| Protections | Death and disability discharge included | Usually lost upon refinancing |

Table 3: Key Differences between Federal Consolidation vs. Private Refinancing

V. Special Situations: School Closures and Taxes

Borrowers often face unique hurdles such as finding student loans after school closure. If your school closed while you were enrolled or shortly after you withdrew, you may be eligible for a closed school loan discharge. To find your student loan information after a school closure, contact your servicer immediately or check the “Closed School” section on StudentAid for a list of affected institutions.

As you resolve issues related to your loan’s status or origin, these records become essential for your annual financial reporting for tax purposes.

For tax season, you will likely need to know where to find my student loan 1098-E form. This form, which reports the interest you paid on your loans, is provided by your servicer. If you had a student loan servicer change during the year, you may need to download a 1098-E from both the old and new servicers to get your total interest deduction.

VI. Frequently Asked Questions

Q: How do I find my student loan repayment plan on StudentAid?

A: Log in to your account and select “View Details” on the “My Aid” dashboard. Your current student loan repayment plan will be listed under the “Loan Details” section for each individual loan. If you don’t see a repayment plan listed on StudentAid, log into your servicer’s website directly or contact them, as they may have the most current information.

Q: How do I find my student loan lender information?

A: In the modern federal system, the ‘lender’ for all Direct Loans is the U.S. Department of Education. However, your “servicer,” the company you actually make payments to and contact for account management, can be found by logging into your dashboard at StudentAid or calling the Federal Student Aid Information Center at 1-800-433-3243 (1-800-4-FED-AID).

Q: How do I know if I have federal or private student loans?

A: Federal loans are listed on your StudentAid profile and are held by the Department of Education. Private loans are not listed there and are typically found on your credit report under the name of a private bank, credit union, or private lender. You can also check your original loan documents (promissory note) or contact your school’s financial aid office for help identifying your loans.

Q: How do I find my student loan account ID?

A: Your Account ID is a unique number (often 10 digits) assigned by your servicer. It is located on your monthly billing statement, your 1098-E tax form, and within the ‘Profile,’ ‘Account Information,’ or ‘Account Summary’ section of your servicer’s online portal. Note that StudentAid does not display your servicer-specific account number. You must get it directly from your servicer’s website or correspondence.

VII. Conclusion

The 2026 student loan environment is defined by a significant narrowing of options, making early identification and strategic action more critical than ever before. With the One Big Beautiful Bill Act (OBBBA) sunsetting legacy income-driven plans like SAVE, PAYE, and ICR, borrowers must be proactive in managing their accounts to avoid being automatically reassigned to plans that may not fit their financial needs.

If you have federal student debt, your immediate priority should be verifying your servicer and student loan identifiers through StudentAid. For Parent PLUS borrowers, the June 30, 2026 consolidation deadline is critical for preserving access to income-driven repayment and forgiveness programs. Other borrowers with FFEL or Perkins loans should consolidate them into Direct Loans to access current federal protections and forgiveness programs even though the one-time payment count adjustment deadline of June 30, 2024 has already passed.

The cornerstone of this new era is the Repayment Assistance Plan (RAP) which will become the primary income-driven option. Crucially, under the RAP, the calculation for your monthly payments is specifically tied to your tax filings, specifically your Adjusted Gross Income, and your family size. It means that your 2025 tax strategy, including deductions and filing status, will directly dictate your student loan costs throughout 2026 and beyond. By staying informed, especially if you are a Parent PLUS borrower who must act by June 30, 2026, or a borrower on SAVE, PAYE, or ICR who must choose a new plan by July 1, 2028, you can ensure that your path toward debt freedom remains secure and predictable.

Related Articles