The 'Wealth Hacker': Paying Off vs. Investing (2026)

Key Terms in This Article

- Capitalization

- When unpaid interest is added to the principal balance of your loan.

- Debt Avalanche

- A repayment strategy focusing on the highest interest rate debt first.

- Debt Snowball

- A repayment strategy focusing on the smallest debt balance first.

- IDR (Income-Driven Repayment)

- A plan that sets your monthly payment based on income and family size.

- RAP (Repayment Assistance Plan)

- The new federal repayment structure introduced in July 2026.

- Servicer

- The company that handles the billing and administration of your loan.

Table of Contents

Key Takeaways

I. Introduction

II. The Great Debate: Should I Pay Off Student Loans or Invest?

- Comparing Loan Interest Rates to Stock Market Returns

- Wealth Building with Student Debt: The Opportunity Cost

III. Fast-Track Strategies: How to Pay Off Student Loans Fast

- Snowball vs. Avalanche: Which Method Wins in 2026?

- Table 1: Aggressive Repayment Mechanics

- The 50/30/20 Rule for Aggressive Student Loan Repayment

IV. Wealth Building Tools for Borrowers

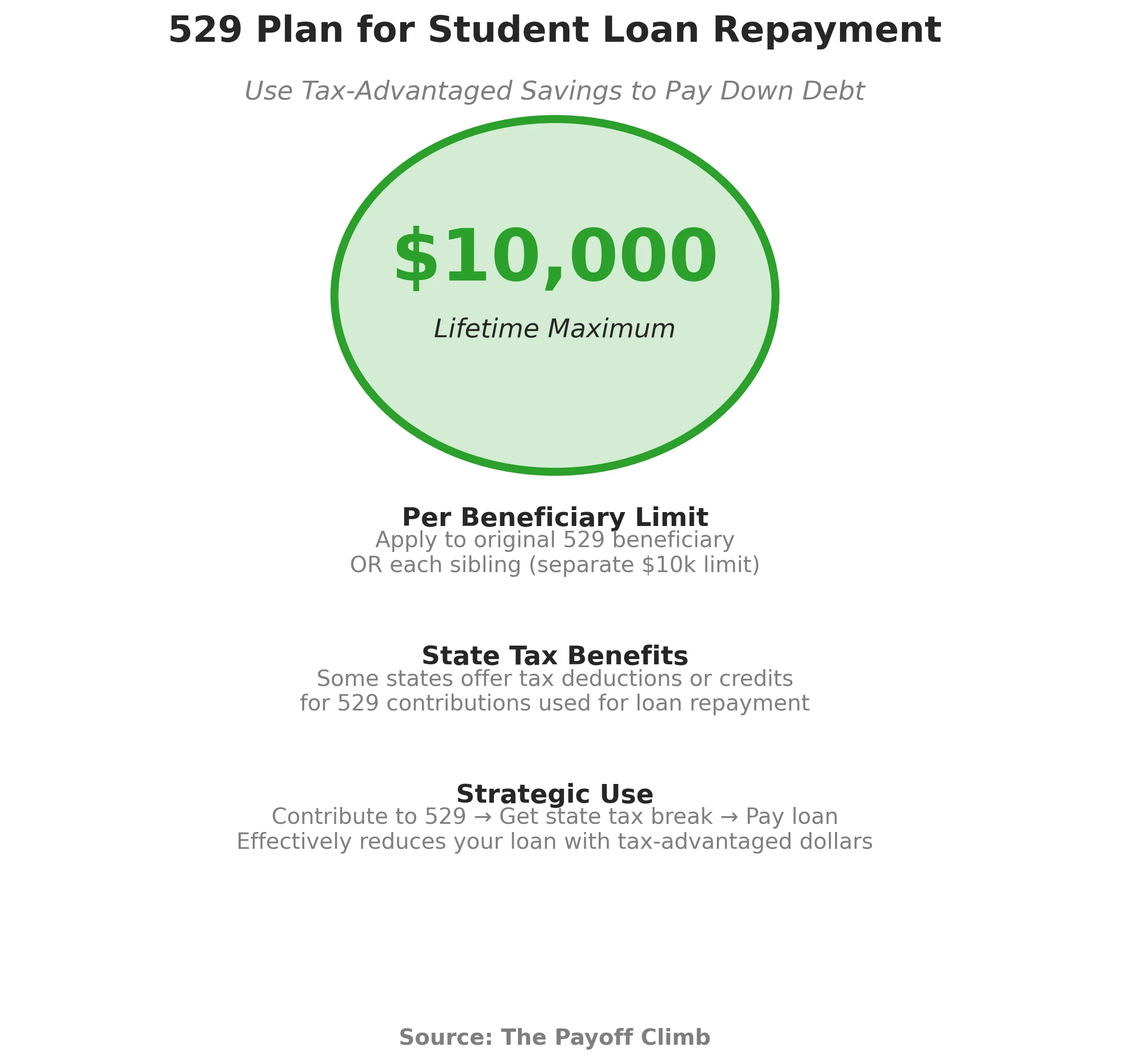

- Using 529 Plans for Loan Repayment (The $10k Rule)

- Using a Roth IRA or 401k to Pay Down Debt

- Credit Card Rewards Strategy

V. Strategic Timing: While In School and Unemployed

- Should I Pay Student Loans While In School?

- How to Pay Off Student Loans While Unemployed

VI. Frequently Asked Questions

VII. Conclusion

Key Takeaways

-

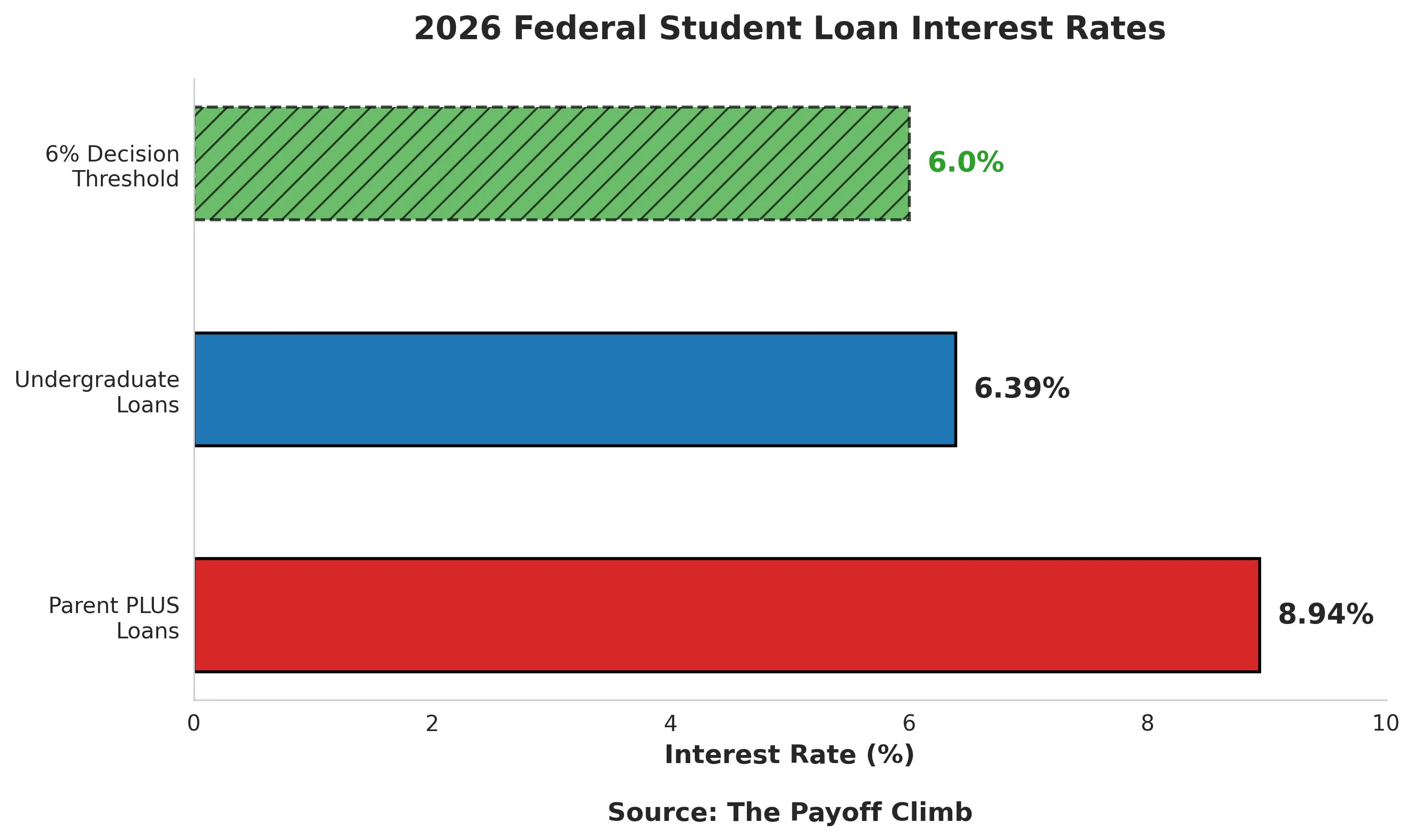

2026 Rates: Undergraduates face 6.39%; Parent PLUS face 8.94%.

-

Total Debt:** The U.S. total is $1.833 trillion as of January 2026.

-

529 Hack:** Use up to $10k tax-advantaged dollars for repayment.

-

Math vs. Mood:** Use the Avalanche for speed and Snowball for motivation.

-

Employer Help:** Many companies now offer student loan matching as a 401k perk.

I. Introduction

The landscape of American education finance has reached a fever pitch in 2026. As of January 2026, total U.S. student debt has hit a staggering $1.833 trillion. For the average undergraduate, this means exiting campus with $39,075 in debt into an economy where interest rates have hit historic highs.

The 2025-2026 academic year saw undergraduate rates climb to 6.39%, while Parent PLUS loans reached a punishing 8.94%. With the sunsetting of the SAVE plan and the introduction of the Repayment Assistance Plan (RAP) on July 1, 2026, borrowers are asking one critical question: Is it better to pay off student loans fast or invest in the market? This guide serves as a source for navigating these waters.

II. The Great Debate: Should I Pay Off Student Loans or Invest?

The choice between debt destruction and wealth accumulation is often framed as a battle between math and psychology. To decide, you must first calculate your “Risk-Free Return.”

Comparing Loan Interest Rates to Stock Market Returns

When you pay down a student loan with a 6.39% interest rate, you are effectively “earning” a guaranteed, risk-free return of 6.39%. In contrast, the stock market offers higher potential returns but comes with volatility.

- A common rule of thumb is the 6% rule: if your loan interest rate is below about 6% and you have a long time horizon, the expected math often favors investing in a diversified portfolio rather than accelerating debt payoff, under typical assumptions about returns, taxes, and risk.

- With current Graduate and Parent PLUS loan rates near 9%, paying off this debt often makes more sense than investing in stocks, because the guaranteed interest savings are comparable to or higher than the after‑tax, risk‑adjusted returns many investors can realistically expect from the stock market.

- For many student loan borrowers, the restart of payments feels like a meaningful pay cut, with research suggesting the median borrower cuts consumption by around 100–150 dollars per month when payments resume.

Wealth Building with Student Debt: The Opportunity Cost

Holding debt is not just a monthly expense; it is a barrier to long-term wealth building.

- Home Ownership: High debt-to-income ratios associated with student loans decrease the likelihood of owning a home and using it to accumulate equity.

- Retirement Prep: Higher debt payments often decrease retirement contributions, making it harder to fully fund retirement accounts.

- Net Worth: For low‑net‑worth households, heavy debt burdens can significantly undermine their ability to build an emergency cushion and positive net worth over time.

III. Fast-Track Strategies: How to Pay Off Student Loans Fast

If you have decided to prioritize debt repayment, 2026 offers several aggressive paths to a $0 balance.

Snowball vs. Avalanche: Which Method Wins in 2026?

These are two of the most commonly discussed strategies in personal finance content:

- The Debt Snowball: You pay off the smallest balance first while maintaining minimums on others. This creates a “psychological win” that fuels momentum.

- The Debt Avalanche: You focus every extra dollar on the loan with the highest interest rate. Mathematically, this generally pays off debt fastest and saves the most interest, assuming all minimums are met for the other loans.

Choosing between the Snowball and Avalanche methods provides you with the mathematical or psychological framework needed to attack debt, but executing that plan requires moving from theory to application. While the strategy dictates which loan you target first, your daily financial habits determine the velocity at which that debt disappears. By integrating specific payment tactics into your chosen method, you can effectively shorten your repayment timeline and minimize the interest that accrues daily.

Once you have selected your strategy, use these specific actions to accelerate your results:

- Lump Sum Payments: Applying “found money” like a tax refund or a work bonus directly to the principal of your target loan provides an immediate reduction in total balance.

- The Side Hustle Sprint: Dedicated gig-economy income, ranging from food delivery to consulting, can be funneled 100% toward your debt to increase monthly payment velocity.

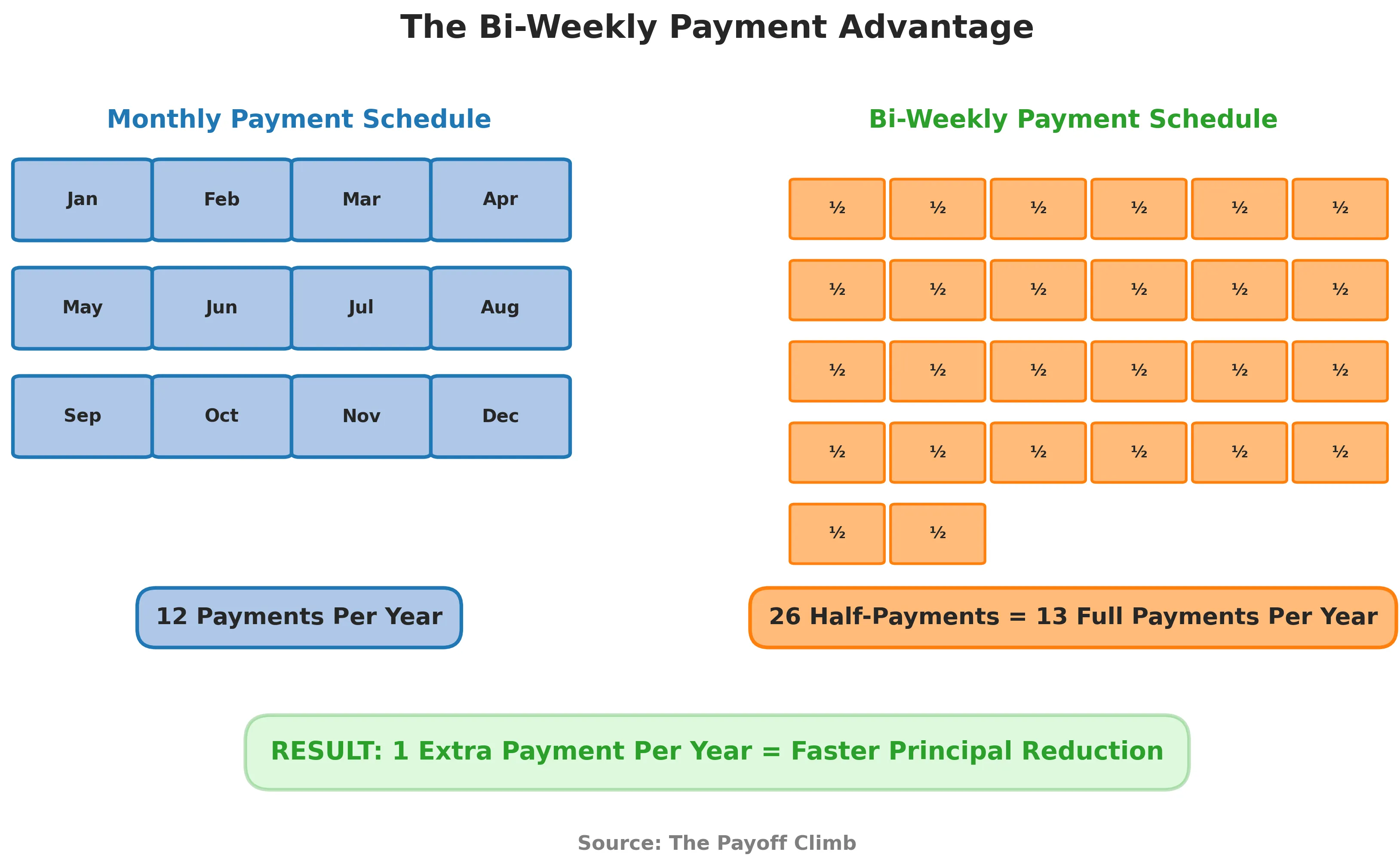

- Bi-Weekly Payment Schedule: By making half-payments every two weeks, you end up making 26 half-payments, which equals 13 full payments a year instead of 12, naturally shaving time off the loan life.

- Daily Interest Targeting: Because federal student loan interest accrues daily using a simple-interest formula, paying earlier (or more often) reduces your principal sooner and can modestly reduce total interest paid, if extra payments are applied to principal.

| Strategy | Action Step | Best For |

|---|---|---|

| Lump Sum | Applying a tax refund or bonus directly to the principal. | Immediate balance reduction. |

| Side Hustle | Repurposing 100% of gig-economy income (after-tax) for debt. | Increasing monthly velocity. |

| Bi-Weekly Payments | Making half-payments every two weeks to hit 13 full payments a year. | Reducing interest accrual. |

Table 1: Aggressive Repayment Mechanics

While these aggressive tactics provide the “how” for your repayment journey, they can only be sustained with a structured “why” in your monthly budget. Relying on sporadic side-hustle income or seasonal windfalls creates inconsistent progress. To truly dominate your debt, you need a predictable framework that balances your lifestyle with your long-term wealth goals. This is where the 50/30/20 rule transforms from a general budgeting tip into a powerful plan to pay off loans, ensuring that your aggressive repayment mechanics are fueled by a steady, reliable percentage of your income every single month.

The 50/30/20 Rule for Aggressive Student Loan Repayment

The 50/30/20 budget serves as a foundational tool for the modern borrower, providing a clear structure to balance mandatory expenses with aggressive wealth-building goals:

- 50% Needs: This category covers your absolute essentials, including housing, utilities, groceries, and your minimum student loan payments to keep your accounts in good standing.

- 30% Wants: These are your non-essential lifestyle choices, such as dining out or subscriptions. Reducing this category even slightly can provide more “fuel” for your debt attack.

- 20% Financial Goals: It should be used to fund your Debt Avalanche or Snowball strategy, making payments above the minimum to crush the principal balance faster.

Once you have mastered the discipline of the 50/30/20 budget, you can begin to look beyond mere repayment and explore the specialized financial instruments that serve as powerful accelerators for your long-term success.

| Category | Allocation | Components & Strategy |

|---|---|---|

| Needs | 50% | Covers absolute essentials: housing, utilities, groceries, and minimum student loan payments to keep accounts in good standing. |

| Wants | 30% | Non-essential lifestyle choices (dining out, subscriptions). Reducing this slightly provides more “fuel” for your debt attack. |

| Financial Goals | 20% | The primary weapon for debt destruction. Use this to fund Debt Avalanche or Snowball strategies by making payments above the minimum. |

Table 2: The 50/30/20 Rule

IV. Wealth Building Tools for Borrowers

Using 529 Plans for Loan Repayment (The $10k Rule)

An often-overlooked tool is the 529 plan. Under current regulations, you can use a 529 plan to pay off up to $10,000 (lifetime limit) of student loans per individual.

- Tax Advantage: In some states, contributions may qualify for a state tax deduction or credit, so you might get a tax break on money you were going to use for debt anyway.

Using a Roth IRA or 401k to Pay Down Debt

While potentially risky, retirement accounts offer specific mechanisms:

- Roth IRA Principal: You can withdraw your original contributions (but not earnings) tax-free and penalty-free at any time to pay off a lump sum.

- 401k Loans: Some qualified plans allow loans up to $50,000, though these are not permitted from IRAs.

- Hardship Distributions: These are generally subject to income tax and a 10% penalty unless specific criteria are met.

Credit Card Rewards Strategy

Most federal student loan servicers and many private lenders do not let you pay student loans directly with a credit card, requiring payment instead from a bank account, check, or similar methods. Third‑party bill‑pay services can charge your credit card and then send a payment to your servicer, but they typically add about a 2–3% fee. Because these fees and normal credit card interest rates often exceed any rewards, and 0% balance‑transfer strategies add fees, time limits, and high default APRs afterward, using credit cards for student loan payments is generally a high‑risk tactic.

V. Strategic Timing: While In School and Unemployed

Should I Pay Student Loans While In School?

While you are not required to pay during at least half-time enrollment, doing so is a major wealth-building move.

- Interest Accrual: Unsubsidized loans accrue interest even while you are in class. Making interest‑only payments during school and grace period can prevent that interest from capitalizing at repayment start.

How to Pay Off Student Loans While Unemployed

If you lose your job and face hardship, do not simply stop paying:

- Unemployment Deferment: You may qualify for an unemployment deferment if you are unemployed or unable to find full‑time work.

- IDR/RAP Plans: If your income is $0, your monthly payment on an Income-Driven Repayment plan could be as low as $0.

VI. Frequently Asked Questions

Q: How do I pay off my student loans fast?

A: In some cases, the quickest way to pay off student loans is the Debt Avalanche method. Focus all extra funds on the loan with the highest interest rate while paying minimums on others. Additionally, apply tax refunds or side hustle income directly to the principal to reduce interest accrual.

Q: Should I pay off student loans or invest in a 401k?

A: First, contribute enough to your 401k to get your employer match, as this often functions like a 100% match on your contribution. After the match, prioritize paying off loans with interest rates above 6%. If your rates are lower, historical stock market returns may favor investing.

Q: Can I use a 529 plan to pay off student loans?

A: Yes, you can use up to $10,000 as a lifetime maximum from a 529 plan to pay down student debt. This applies to both the original beneficiary and their siblings. Some states offer tax incentives for these contributions, providing a double benefit.

Q: Are student loans worth it in 2026?

A: Federal student loans offer protections like Income-Driven Repayment and Public Service Loan Forgiveness (PSLF) that private loans do not. However, with 2026 interest rates hitting 6.39% to 8.94%, consider scholarships or employer reimbursement for educational purposes.

VII. Conclusion

Navigating student debt in 2026 requires a shift from passive repayment to active financial management. With total U.S. student debt reaching $1.833 trillion and interest rates for Parent PLUS loans climbing to 8.94%, the cost of inaction has never been higher. Whether you choose the mathematical efficiency of the Debt Avalanche or the psychological momentum of the Debt Snowball, the goal is to reduce the principal balance as quickly as possible to avoid the long-term drag on wealth accumulation.

The introduction of the Repayment Assistance Plan (RAP) on July 1, 2026, alongside existing tools like the $10,000 lifetime 529 plan provision, provides a robust toolkit for the modern borrower. By integrating these strategies with a disciplined 50/30/20 budget, you can effectively attack debt and begin the transition toward meaningful net worth growth.